As individuals navigate their retirement years, it becomes essential to understand the various factors that impact Medicare premiums, such as: earned income, self-employment income, investments, real estate, rental income, retirement withdrawals, Social Security, and pensions. In this article, we will explore the relationship between Medicare premiums and how Required Minimum Distributions (RMDs) can affect retirement income planning and healthcare costs.

Required Minimum Distributions (RMDs)

The age for RMDs has recently changed due to SECURE Act 2.0. The current age to begin RMDs has been increased to age 73 starting in 2023 (up from age 72). RMDs will increase to age 75 starting in 2033.

RMDs only require withdrawals from traditional funds whether that is a 401(k), TSP, IRA, or other traditional type retirement plan. Roth funds are NOT subject to RMDs.

Medicare Part B & D Premiums are Based on Income

RMDs Pushing You Into Higher Medicare Part B & D Premiums

Prior to receiving RMDs, you may have been enjoying a nice retirement between Social Security, pension, and maybe a small withdrawal from the retirement account here and there. Left unchecked, the money in the traditional IRA is growing and compounding over the years. Looming in the background are RMDs that can launch you into a higher tax bracket and increase the annual cost of health insurance. Proper knowledge of how RMDs work and a plan to lower a future RMD burden can help prevent this.

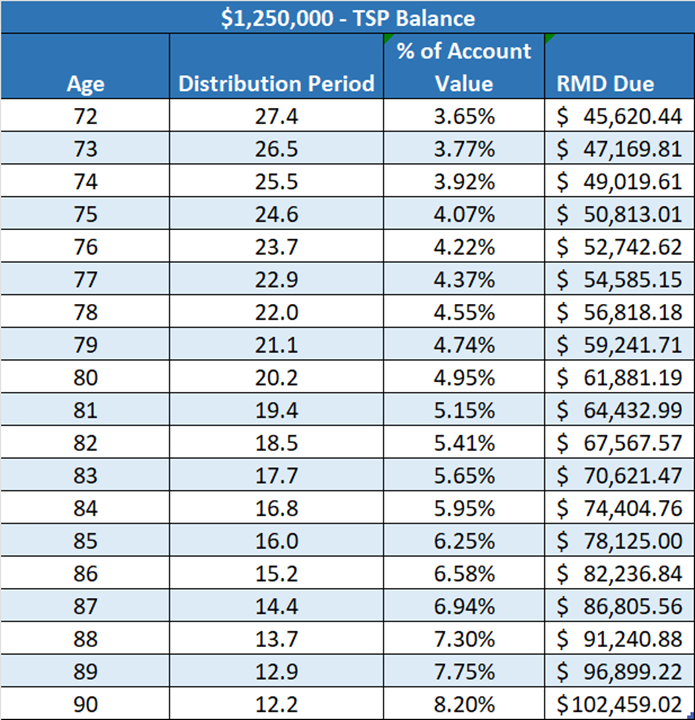

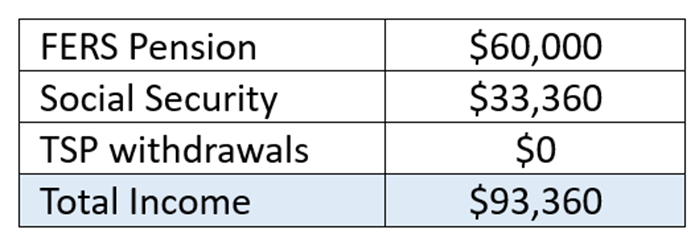

Let’s say you are a single, retired FERS annuitant and age 65. You are receiving a $5,000/month FERS pension, $2,780/month for Social Security, and taking no withdrawals from a TSP that is valued at $1,250,000.

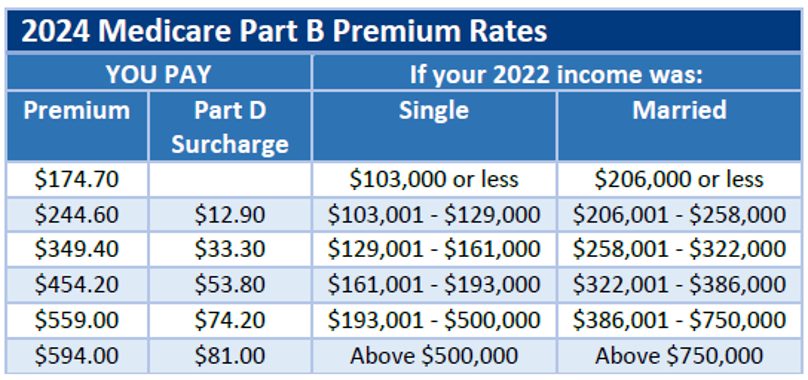

Your total income would place you in the lowest Medicare Part B premium at $174.70/month and $0/month for Part D.

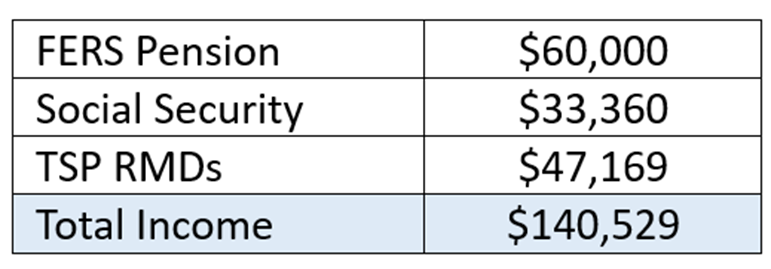

If we swap the ages from 65 to 73, the Medicare Part B premium jumps to $349.40/month for Medicare Part B and $33.30/month for Part D. That’s almost $2,500/year MORE for the same health coverage.

This is a simple explanation of how RMDs can increase health insurance in the future. The most likely scenario may be even worse. A balanced investment strategy will generally outgrow inflation and withdrawals in the retirement account. In the previous example of the 65-year-old retiree, let’s assume the TSP is growing at a rate of 6% with no withdrawals until age 73. The account value will have grown from $1,250,000 to $1,992,310 at age 73. The RMD is much larger now.

The TSP will not stop growing if you have the funds invested and are taking no or moderate withdrawals. The compounding growth over the years will balloon the RMD down the road. Yes, Medicare income brackets will increase but usually matched with inflation. The goal of an investment strategy is to keep up with inflation and hopefully exceed inflation in the long-term. In this scenario, your Medicare Part B premium is now $454.20/month and Part D is $53.80/month which is an increase of $4,000/year.

What Can You Do?

There are some strategies to reduce health insurance premiums and taxes down the road. Conducting Roth conversions is a great way to reduce RMDs in the future as Roth IRAs do not have RMDs. Making small systematic withdrawals below higher tax brackets. If you are charitable, the use of a Qualified Charitable Distribution (QCD) will reduce income while giving to a charitable cause. There is also the Qualified Longevity Annuity Contract (QLAC) that can avoid taking RMDs until age 85.

Important!

Federal employees should take the time to understand their decision on whether to take Medicare Part B or not at age 65. If you will be falling into a premium of $349.40 or higher you may not see the financial incentive of taking Part B. Proper planning now will help you understand what your income is now and into the future which can help you save thousands of dollars down the road.

Reach Out to Us!

If you have additional federal benefit questions, reach out to our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciary (AIF®) professionals. At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Interested in having PlanWell host a federal retirement seminar for your agency? Reach out, and we can collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and schedule a one-on-one meeting with a ChFEBC today.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.