Benefits of Investing in TSP

Investing in the TSP offers multiple benefits. These include reduced administrative costs compared to typical mutual funds, tax advantages, and matching contributions for federal employees. In addition, TSP funds tend to have lower expense ratios, making them a cost-effective way to invest. The ability to track the TSP plan performance and TSP fund returns provides participants with transparency, allowing them to adjust their investment strategies as needed to grow their TSP balances effectively.

Pros and Cons of Thrift Savings Plan

The are many advantages and disadvantages of TSP. To learn more we have written an articles that outlines the pros and cons of TSP.

Should You Transfer Out of Thrift Savings Plan (TSP)?

How Do TSP Fund Returns and Share Price History Affect My Savings?

Understanding Share Price History

Share price history is vital for analyzing how a particular TSP fund has performed over time. This history can indicate how the fund’s value has fluctuated due to market conditions and investment strategies. For example, the TSP C Fund, which tracks the S&P 500 index, may show significant growth during a bull market period. Examining the share price history helps participants understand the volatility and long-term potential of their TSP investments.

How to Measure TSP Fund Performance

Measuring TSP fund performance involves analyzing the rate of return over various periods, taking into account dividends, interest, and other earnings. Tools and resources provided by the TSP, such as TSP performance today reports, can be very useful. Participants need to consider both short-term and long-term performance when making decisions, particularly when planning for retirement. Comparing TSP investment funds performance across different periods and against benchmarks helps in assessing the effectiveness of their investment strategy.

Impact of Performance on Retirement Savings

The rate of return of TSP funds directly impacts retirement savings. Higher returns mean greater growth potential, which is crucial for ensuring that savings grow enough to offset inflation and support a comfortable retirement. Participants must consider the performance of their chosen funds carefully, as poor performance can significantly reduce the retirement income. Regularly reviewing TSP fund performance, like TSP C Fund performance 2023 or TSP I Fund performance, ensures that participants are on track to meet their retirement goals.

How Is the C Fund TSP Performance in 2024?

Overview of the C Fund

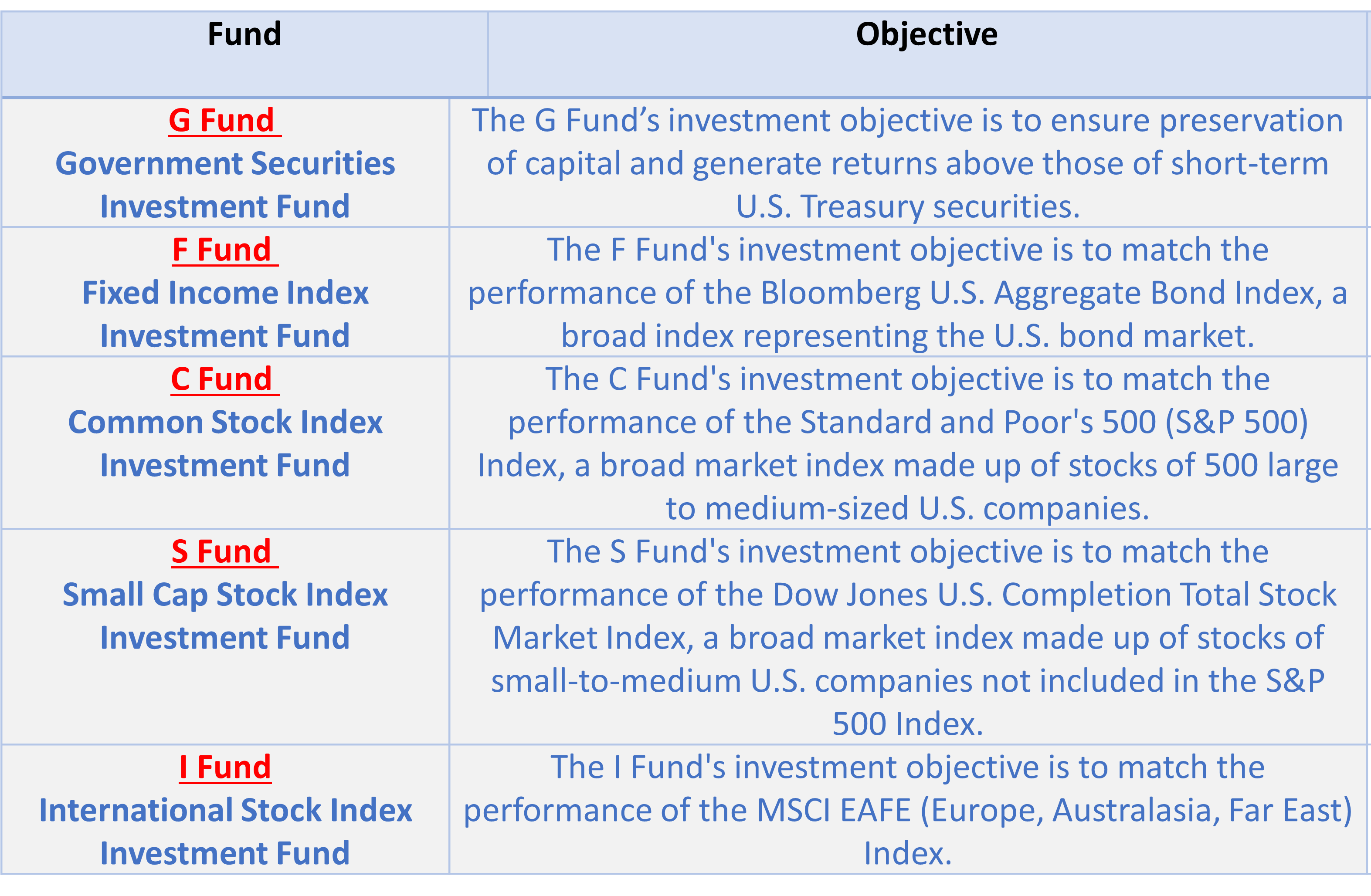

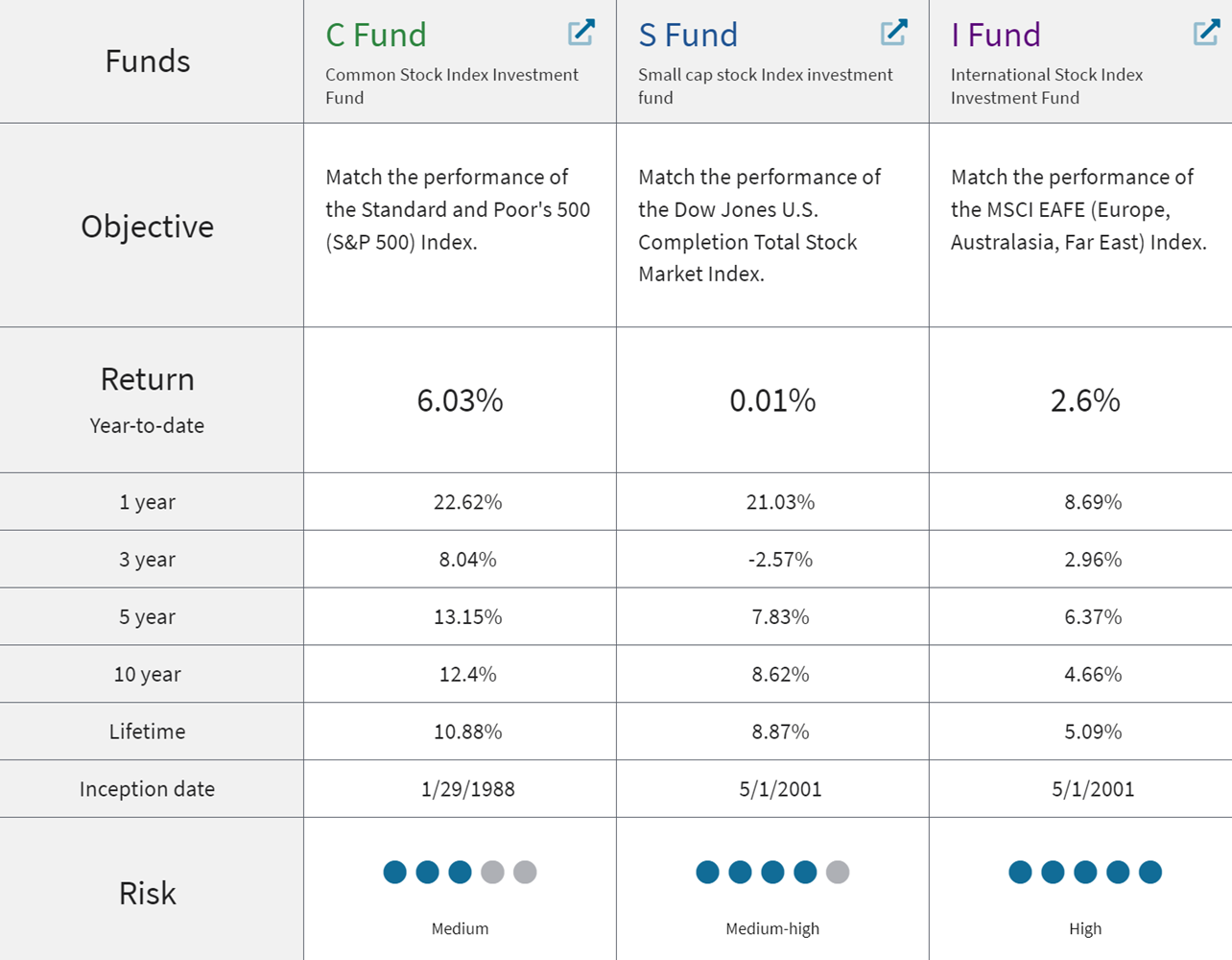

The C Fund invests in common stocks of large U.S. companies and aims to match the performance of the S&P 500 Index. As one of the most popular TSP funds, it offers the potential for high returns due to its exposure to the broader market. However, with this potential comes increased volatility compared to more conservative funds. Federal employees and members relying on the C Fund need to stay updated on its performance and adjust their investment strategies accordingly.

2024 Performance Analysis

In 2024, tracking the C Fund TSP performance involves analyzing its quarterly and annual returns, taking into account broader economic conditions and market trends. The performance of the TSP C Fund can be significantly affected by factors like inflation, interest rates, and corporate earnings reports. Understanding the underlying forces behind the C Fund’s performance helps participants make informed decisions about their allocations and potential adjustments needed in their TSP strategies.

Comparing with Other TSP Funds

Comparing the TSP C Fund performance 2024 with other TSP funds helps investors understand where the C Fund stands in relation to safer or more aggressive options. For example, during periods of high inflation, the G Fund might be seen as a safer investment, while the I Fund offers diversification through international exposure. By evaluating relative performance, participants can better fine-tune their portfolios to balance growth and risk, ensuring their TSP investments are well-positioned for their financial goals.

What Are the Differences Between the L Income Fund and the G Fund?

Understanding the L Income Fund

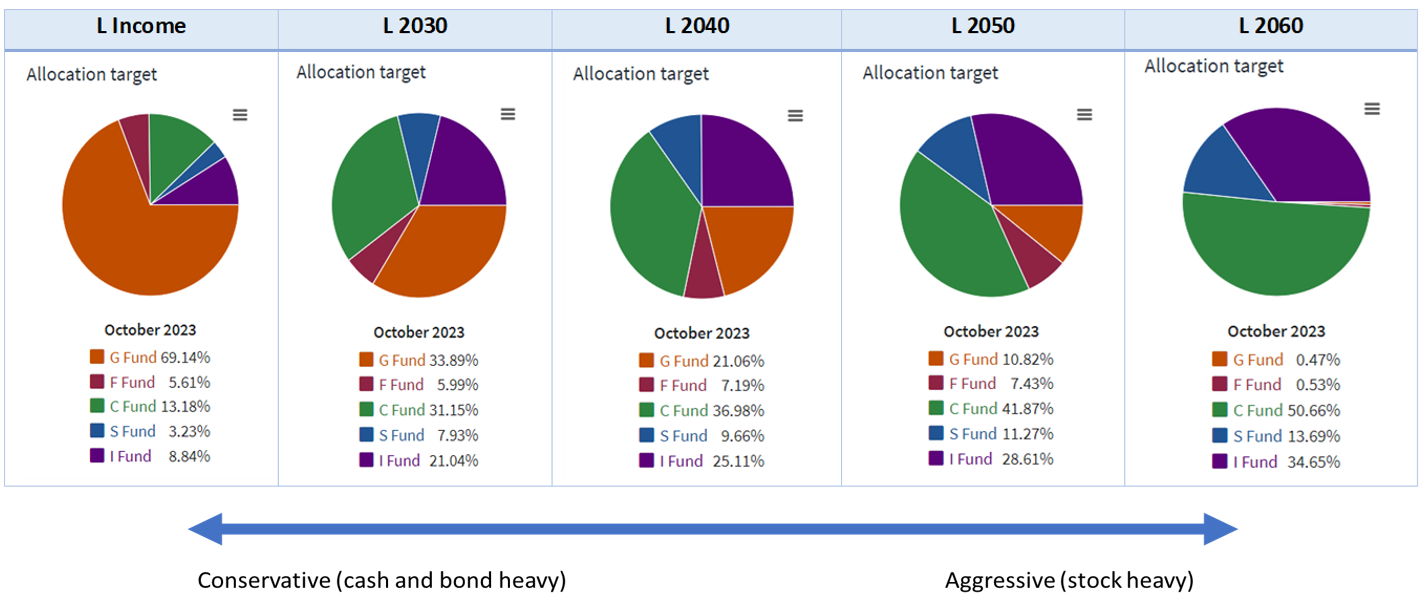

The L Income Fund is one of the TSP’s Lifecycle funds aimed at participants who are already withdrawing or expect to begin withdrawing their TSP account in the near future. This fund is designed to provide income and stability, with a conservative mix of TSP funds. Understanding the L Income Fund’s performance and allocation helps participants make decisions about using it to stabilize their retirement income.

Exploring the G Fund

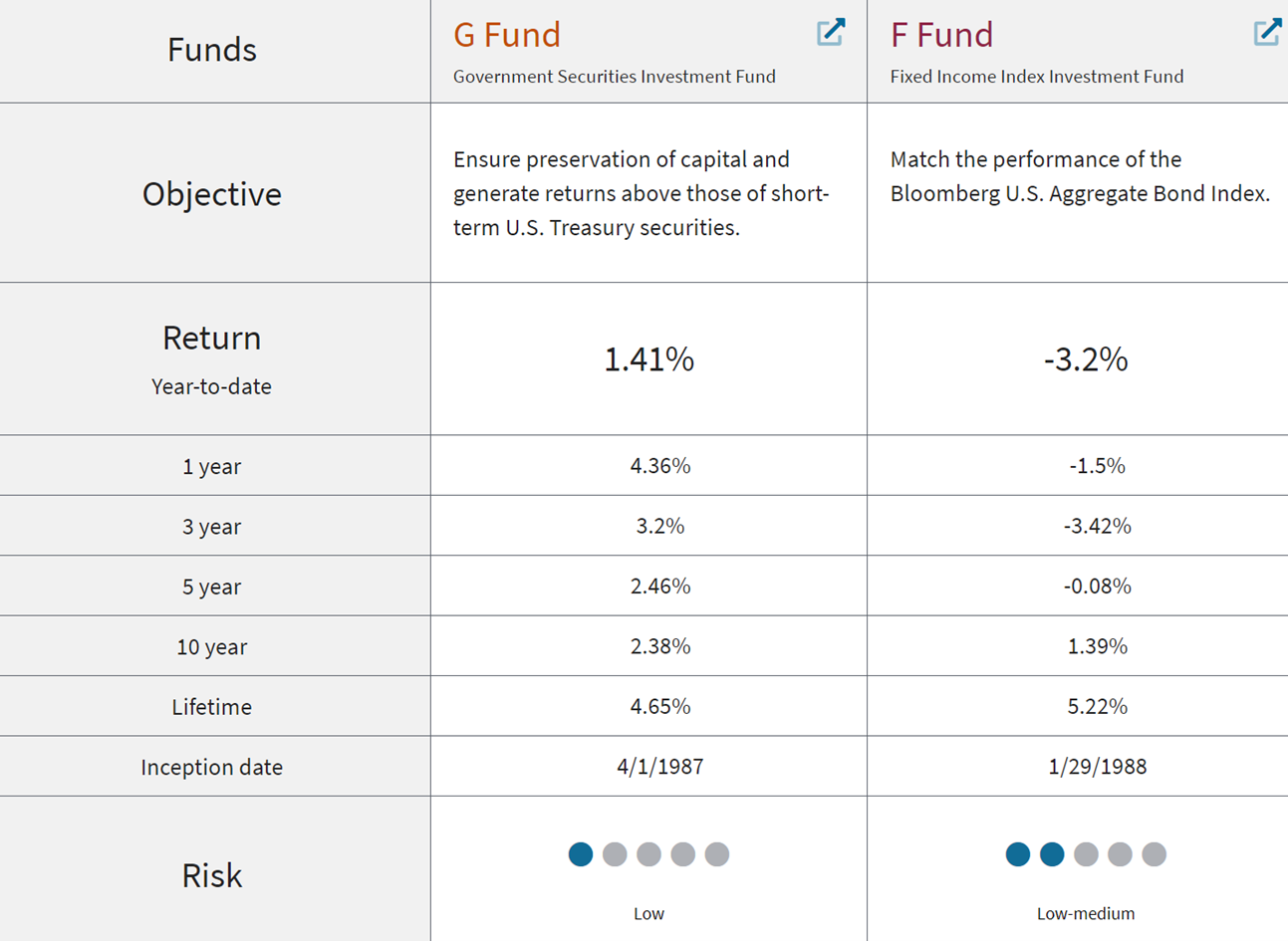

The G Fund invests in government securities and aims to provide a rate of return higher than inflation while avoiding the risk of loss. The TSP G Fund rate today makes it an attractive option for risk-averse investors seeking stable returns. Since the G Fund is backed by the U.S. government, it offers security and reliability, but its returns may be lower compared to more aggressive funds like the C or S Fund.

L Income Fund vs. G Fund: Which Is Better for Retirement Savings?

Choosing between the L Income Fund and the G Fund depends on individual financial goals and risk tolerance. The L Income Fund offers a balanced approach by combining different TSP funds, providing some growth potential with reduced risk. It can be a useful tool for participants seeking a diversified strategy. Conversely, the G Fund’s stability is ideal for those prioritizing capital preservation. Examining the performance, risk factors, and expected returns of both funds helps federal employees decide which option aligns better with their retirement savings strategy.