Understanding Inherited IRA Rules and TSP Beneficiaries: Estate Planning for Federal Employees

When federal employees, retirees, and family members are developing an estate plan, understanding the difference between types of beneficiaries and beneficiary accounts both in and outside of the Thrift Savings Plan (TSP) can be key in ensuring a proper estate plan is in place. This article will review an overlooked tax problem with the TSP and also what happens with an inherited IRA that could help your heirs dodge a major tax liability.

Need to Learn More about Inherited IRA Withdrawal Rules? Schedule a 1-on-1 meeting with a PlanWell Advisor.

Inheriting IRA Funds vs. Traditional TSP Funds: What Beneficiaries Need to Know

Primary and Non-Primary Beneficiaries in TSP are Not Taxed the Same

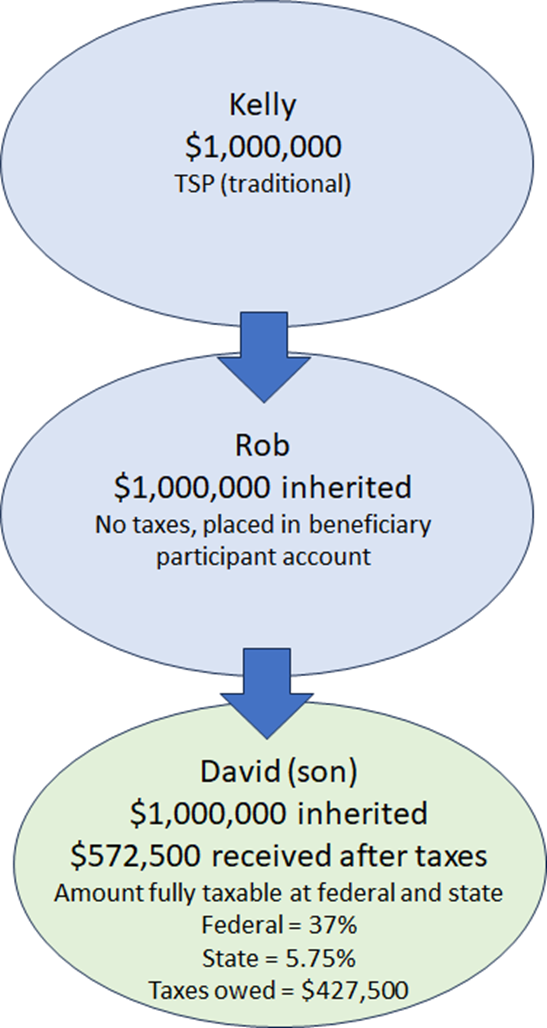

Because primary beneficiaries of an inherited TSP account can keep their funds in the federal savings plan without seeing tax consequences until they take required minimum distributions (RMDs), they often think this is the same for whoever inherits the money after them. But unlike IRA assets, this is not the case. Non-primary beneficiaries who inherit TSP money have 90 days to decide how they would like to distribute the the cash before it subject to federal and state taxes and disbursed. This money cannot be rolled over into an original IRA or an inherited IRA at this point, most likely leaving them with a significant tax burden. Unlike funds in a traditional IRA, they must take a lump-sum distribution from the TSP that could be greatly reduced by taxes, as seen in the infographic below:

[image]

Estimate future TSP value with our Thrift Savings Plan calculator.

Key Takeaway: Verify Your Estate Plan Before it is Too Late

Talking with an estate planner or a financial advisor that works with federal employees can be advantageous when developing a proper estate plan. One of the easiest ways to avoid this tax burden is to withdraw money out of the TSP to a private IRA after retiring from the federal government. Verify your estate and financial plans with a trusted professional to ensure your heirs are protected.

Close to retirement from the federal government? Attend an online Federal Retirement Workshop

What Happens When You Inherit an Individual Retirement Account (IRA)?

How Do Inherited Traditional IRAs Differ from Traditional IRAs?

Inherited IRAs differ significantly from traditional IRAs in terms of rules and management. When you inherit an IRA, you do not have the same flexibility as the original account holder. Unlike a traditional IRA, where the account owner can make contributions and withdrawals at their discretion, an inherited IRA comes with specific distribution rules. Beneficiaries must adhere to these rules, which often include required minimum distributions (RMDs) that must be taken annually. The inherited IRA cannot be treated as your own, meaning you cannot contribute to it or roll it over into your own IRA account. Understanding these differences is crucial for beneficiaries to avoid penalties and optimize their inheritance.

How Does the 10-Year Rule Apply to Inherited IRAs?

The 10-year rule is a significant change in the management of inherited IRAs, introduced by the SECURE Act. Under this rule, most non-spouse beneficiaries must deplete the inherited IRA within 10 years following the year of the original account owner's death. This rule applies to both traditional and Roth IRAs. Unlike the previous stretch IRA rules, which allowed beneficiaries to take distributions over their lifetime, the 10-year rule requires that all funds be withdrawn by the end of the 10th year. This can have substantial tax implications, as beneficiaries may face higher income tax rates if large distributions are taken in a single year.

How Do Withdrawal Rules Affect Inherited IRAs?

What Are the Required Minimum Distribution (RMD) Rules?

RMD rules are a critical aspect of managing inherited IRAs. For traditional IRAs, beneficiaries are generally required to take RMDs starting the year following the year of the IRA owner's death. The amount of the RMD is calculated based on the beneficiary's life expectancy and the account balance. Failure to take the RMD can result in a hefty penalty, amounting to 50% of the required distribution. In contrast, inherited Roth IRAs do not have RMDs for the original owner, but beneficiaries must still adhere to the 10-year rule for distributions.

Who is the Beneficiary of the IRA? Withdrawal Rules Differ for Spouses

Spouse beneficiaries have more flexibility compared to non spouse IRA beneficiaries when it comes to inherited IRAs. A spouse can choose to treat the inherited IRA as their own, allowing them to defer RMDs until they reach the age of 72. Alternatively, they can roll over the inherited IRA into their own retirement account, such as a traditional IRA or a Roth IRA. This option can be beneficial if the spouse is younger than the IRA owner, as it allows for continued tax-deferred growth. Spouses can also opt to move the assets into an inherited IRA, sometimes called a beneficiary IRA, and follow the standard RMD rules applicable to non-spouse beneficiaries.

What Are the Tax Implications of Withdrawals from Inherited Account?

Withdrawals from inherited IRAs can have significant tax implications. For traditional IRAs, distributions are generally subject to income tax, as the funds were contributed pre-tax. This means that beneficiaries must report the withdrawals as income on their tax returns. In contrast, withdrawals from inherited Roth IRAs are typically tax-free, provided the account has been open for at least five years. However, beneficiaries must still adhere to the 10-year rule for distributions. Understanding these tax rules is essential for beneficiaries to plan their withdrawals strategically and minimize their tax liability.

What Are the Options for Spouses Inheriting an IRA?

Can a Spouse Convert an Inherited IRA to a Roth IRA?

Spouses have the unique option to convert an inherited IRA to a Roth IRA. This conversion can be advantageous if the spouse expects to be in a higher tax bracket in the future, as it allows for tax-free growth and withdrawals in retirement. However, the conversion is subject to income tax on the amount converted, so it is essential to consider the immediate tax implications. Spouses should evaluate their current and future financial situation to determine if a Roth conversion aligns with their retirement planning goals.

What Are the Benefits of Rolling Over an Inherited IRA?

Rolling over an inherited IRA into a spouse's own IRA can offer several benefits. It allows the spouse to consolidate retirement accounts, simplifying management and potentially reducing fees. Additionally, it enables the spouse to defer RMDs until they reach the age of 72, providing more time for the assets to grow tax-deferred. This option also allows the spouse to continue making contributions to the IRA, further enhancing their retirement savings. However, it is crucial to weigh these benefits against the potential tax implications of a rollover.

How Does a Spouse's Age Affect Inherited IRA Decisions?

A spouse's age plays a significant role in determining the best course of action for an inherited IRA. If the spouse is younger than the IRA owner, they may benefit from rolling over the inherited IRA into their own account, allowing for continued tax-deferred growth. Conversely, if the spouse is older, they may prefer to open an inherited IRA and begin taking RMDs, especially if they need the income. The decision should be based on the spouse's overall retirement plan, financial needs, and tax considerations.

Rules and Advantages When You Inherit a Roth IRA

What Are the Distribution Rules for Inherited Roth IRAs?

Inherited Roth IRAs have specific distribution rules that beneficiaries must follow. While the original account owner is not required to take RMDs, beneficiaries must deplete the account within 10 years following the year of the owner's death. This rule applies regardless of the beneficiary's relationship to the deceased. Unlike traditional IRAs, distributions from inherited Roth IRAs are generally tax-free, provided the account has been open for at least five years. Beneficiaries should plan their withdrawals carefully to maximize the tax-free benefits of the inherited Roth IRA.

RMDs and Taxation: Distribution Rules that Apply to Inherited Roth IRAs

While the original owner of a Roth IRA is not subject to RMDs, beneficiaries must adhere to the 10-year rule for inherited Roth IRAs. This means that the entire account balance must be distributed by the end of the 10th year following the year of the death of the IRA owner. Although there are no annual RMDs, beneficiaries should consider the timing of their withdrawals to optimize the tax-free growth potential of the account. Strategic planning can help beneficiaries make the most of their inherited Roth IRA. Inherited Roth IRAs offer significant tax advantages, as distributions are generally tax-free. This is because the original contributions were made with after-tax dollars, and the account's growth is tax-exempt. However, to qualify for tax-free withdrawals, the account must have been open for at least five years. Beneficiaries should be aware of this requirement to avoid unexpected tax liabilities. By understanding the tax rules associated with inherited Roth IRAs, beneficiaries can effectively manage their inheritance and maximize their financial benefits.

What Should Eligible Designated Beneficiaries Know?

Who Qualifies as an Eligible Designated Beneficiary?

Eligible designated beneficiaries are a specific category of individuals who have more favorable distribution options for inherited IRAs. This group includes the surviving spouse, minor children of the deceased, disabled or chronically ill individuals, and beneficiaries who are not more than 10 years younger than the IRA owner. These beneficiaries can take advantage of the stretch IRA provisions, allowing them to take distributions over their life expectancy rather than adhering to the 10-year rule. Understanding who qualifies as an eligible designated beneficiary is crucial for optimizing the management of inherited IRAs.