July 2024 G Fund Rate Today

TSP G Fund: Understanding the Government Securities Investment Option in the Thrift Savings Plan

The Thrift Savings Plan (TSP) is a retirement savings plan for federal employees and members of the uniformed services, offering a variety of investment funds to help individuals plan for their retirement. Among these options, the TSP G Fund stands out as a unique and secure investment choice. The G Fund is an integral part of the TSP, designed to provide a stable and low-risk investment option for participants. This article aims to delve into the complexities of the TSP G Fund, explaining its characteristics, yield and return dynamics, security features, and strategies for maximizing returns.

How does the TSP G Fund Yield and Return work?

What determines the TSP G Fund Yield?

The TSP G Fund yield, essentially the rate of return on the investment, is determined by the interest rates of the U.S. Treasury securities specifically issued to the TSP. These rates are based on the average market yields of U.S. Treasury securities with four or more years of maturity, adjusted to match the maturity of a one-day security. Therefore, changes in federal interest rates and broader economic conditions directly influence the monthly G Fund yields experienced by investors.

How is the G Fund Rate of Return calculated?

The rate of return for the TSP G Fund is calculated by taking the monthly interest income generated by the assets held in the fund and dividing it by the fund’s asset value at the start of the month. This provides a monthly rate which can be annualized to understand the yearly performance. The TSP G Fund return rates are published regularly by the TSP, reflecting current economic conditions and U.S. Treasury interest rates.

What is the current TSP G Fund Rate Today?

4.625%

An easy way to find the G fund rate today is by looking at the current TSP loan interest rate. You can find those rates here: Current TSP Loan Interest Rate.

As of the latest data available, the TSP G Fund rate today is influenced by prevailing Treasury interest rates. This rate can fluctuate monthly based on changes in the broader economic environment and federal monetary policy. For the most up-to-date information on the current TSP G Fund rate, TSP participants should refer to the latest TSP Fund performance reports and updates provided by the Federal Retirement Thrift Investment Board (FRTIB).

Knowledge is Confidence!

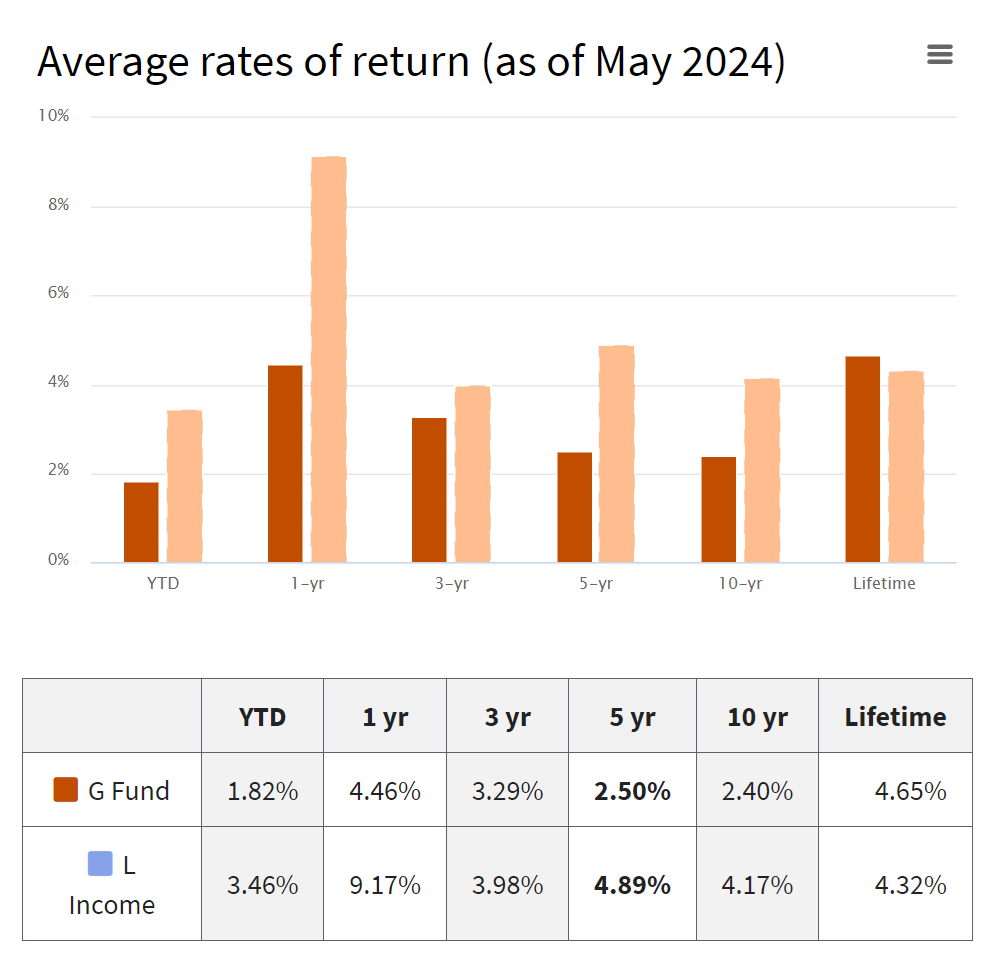

G Fund TSP Returns

The historical G fund TSP returns are incldued below. These returns show the 1, 3, 5, 10, and life of the G fund TSP returns. As of June 2024, the TSP G fund rate today is 4.625% which is the highest we have seen since 2007. Time will tell if the higher level of rates in the G fund will continue.

What is the TSP G Fund?

What’s the historical context of the TSP G Fund?

The TSP G Fund, or Government Securities Investment Fund, was created to offer a risk-free investment option for federal employees and members of the uniformed services. Established as part of the Federal Employees’ Retirement System Act of 1986, the G Fund invests in short-term U.S. Treasury securities specifically issued to the TSP. The primary intent behind the G Fund’s creation was to provide TSP participants with a secure investment option that protects their principal while offering a guaranteed rate of return.

What are the primary characteristics of the TSP G Fund?

The TSP G Fund’s primary characteristic is its low-risk nature. It is backed by the full faith and credit of the U.S. government, which assures that the principal is always protected. The G Fund invests exclusively in non-marketable U.S. Treasury securities that are specially issued to the TSP. As a result, the G Fund’s rate of return is sensitive to interest rates on the short-term federal debt but still offers a higher rate than most other short-term government securities available to the public.

How does the TSP G Fund compare to other TSP Investment Funds?

Compared to other TSP investment funds, the G Fund provides the highest degree of security and stability. While other TSP funds, such as the C, S, I, F, and L funds, involve varied levels of risk associated with stock and bond markets, the G Fund’s returns are not subject to market volatility. This makes the G Fund an attractive option for risk-averse investors looking to preserve their capital while earning a steady return. The trade-off, however, is typically lower long-term growth potential compared to the more aggressive funds.

Why is the TSP G Fund considered a secure investment?

What makes the G Fund risk-free?

What makes the G Fund risk-free is its unique investment in short-term U.S. Treasury securities that are guaranteed by the U.S. government. This means that both the principal and interest payments are backed by the U.S. government’s credit, effectively eliminating the risk of default. Unlike other investment options that can lose value due to market fluctuations, the G Fund securities are immune to market risk and interest rate risk, providing a stable and reliable investment vehicle.

How does the G Fund performance compare against other secure TSP Funds?

The G Fund performance is consistently stable, making it a benchmark for security among TSP investment options. Other secure TSP funds, like the F Fund, which invests in fixed-income securities, still carry some level of risk due to potential interest rate changes and credit defaults. In contrast, the G Fund’s performance remains unaffected by these factors, providing a constant and predictable return. Historically, the G Fund does not offer the highest returns but compensates with unparalleled security and steadiness, which is vital for conservative investors.

What is the historical performance of the G Fund?

Historically, the G Fund has offered modest but consistent returns, generally ranging between 1% and 2.5% annually over the past decade, as highlighted in various TSP G Fund news articles. The historical performance of the G Fund reflects its role as a safe harbor for retirement investors seeking to protect their principal. While the returns may be lower compared to equity funds during bullish markets, the G Fund remains an invaluable component of a diversified retirement strategy, particularly during economic downturns.

What happens to the TSP G Fund during a debt ceiling suspension?

What does it mean for the G Fund to be suspended?

A debt ceiling suspension implicates the legal limit on the total amount of federal debt that the government can issue is temporarily lifted or paused. During such events, the G Fund can be temporarily impacted, as the U.S. Treasury may prioritize the management of the overall debt. TSP participants may hear about the G Fund being temporarily suspended or “disinvested” as part of Treasury’s efforts to avoid exceeding the debt limit. However, the principal and earned interest are still safeguarded by federal law, ensuring G Fund investors do not lose their investments.

How are TSP Accounts affected when the G Fund is disinvested?

When the G Fund is disinvested during a debt ceiling crisis, the Treasury Department essentially borrows from the G Fund to manage government operations. However, TSP accounts themselves remain unaffected in terms of the nominal balance and credited earnings. The fund account balances will continue reflecting the value as if the disinvestment did not occur. Once the debt ceiling issue is resolved, the Treasury is legally required to fully restore any disinvested amounts, ensuring no G Fund investor faces any loss.

What is TSP G Fund Disinvestment?

Disinvestment of the TSP G Fund occurs when the U.S. Treasury reallocates funds from the G Fund to cover other obligations during periods when it’s unable to issue additional debt due to the debt ceiling. Although this might sound alarming, the practice is temporary and does not impact the security of the invested principal or accrued interest. TSP participants’ account balances and G Fund returns continue to be recorded as if the disinvestment never took place.

How can investors maximize their returns with the TSP G Fund?

What strategies should be considered for higher G Fund Returns?

To maximize returns from the TSP G Fund, investors should focus on the timing and duration of their investments. While the G Fund provides a stable return, it is beneficial to pair it with other TSP investment funds that offer higher growth potential. By strategically reallocating funds between the G Fund and higher-performing equity funds, investors can enhance overall FRTIB performance while maintaining a balanced risk profile.

What role do Lifecycle Funds play in optimizing G Fund investments?

Lifecycle Funds, or L Funds, are designed to balance risk and return by automatically adjusting the composition of investments as investors approach retirement. Incorporating the G Fund as a part of these Lifecycle Funds ensures that a portion of the portfolio remains secure, particularly as participants age and become more risk-averse, leveraging the stability highlighted in TSP G Fund news. This automatic rebalancing can optimize returns while gradually reducing exposure to market volatility, enabling a smoother transition into retirement.

How can withdrawals from the TSP G Fund impact overall performance?

Withdrawals from the TSP G Fund should be managed carefully to sustain overall portfolio performance. Premature or large-scale withdrawals can reduce the compounding benefit of accrued interest. It’s advisable to plan withdrawals strategically, especially during periods of economic uncertainty, to maintain the stability and growth of retirement savings. Consulting with a financial advisor can help TSP investors develop a withdrawal strategy that aligns with their long-term financial goals.

GFund Rate

To find the historical rates of return for GFund rate of return you can find more information at TSP’s website: TSP Individual Funds (GFund rate)

TSP G Fund Suspended

In 2023, the TSP G fund was suspended due to the debt limit. Learn more about the TSP G fund suspension in the article written to congress here: Letter to Congress.

TSP G Fund Rates of Return

What does the future of the TSP G fund rates of return look like? As of July 2024, the G Fund rate of return, currently at 4.625%, is the highest it has been in a number of years. The G fund rate has declined from 4.75% in July 2024 due to the anticipation that the Federal Reserve will begin to cut interest rates later in the year.

Reach Out to Us!

If you have additional federal benefit questions, contact our team of CERTIFIED FINANCIAL PLANNER™ (CFP®) and Chartered Federal Employee Benefits Consultants (ChFEBC℠). At PlanWell, we are federal employee financial advisors with a focus on retirement planning. Learn more about our process designed for the career fed.

Preparing for federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars here! Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out, and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting here.