Retirement Options for Federal Employees Considering Trump Buyout for "Deferred Resignation"

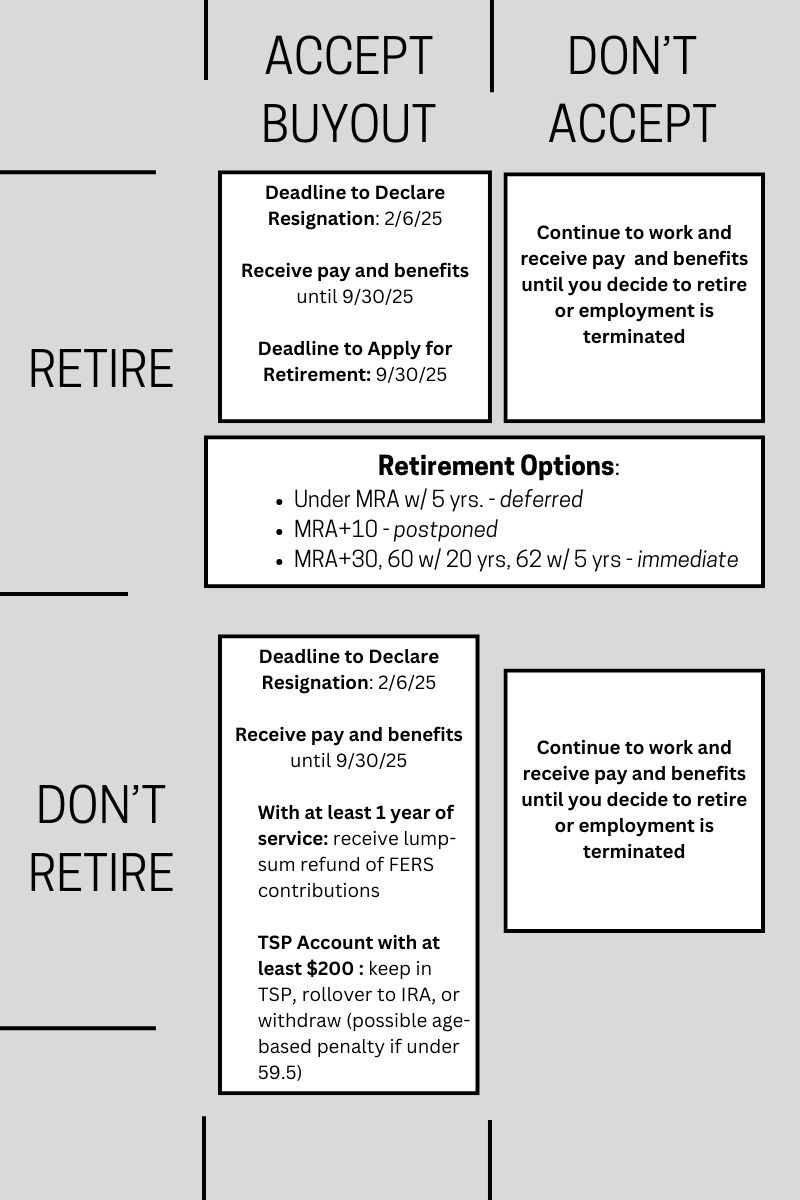

The deferred resignation letter sent to federal employees this week has imposed a strict deadline of February 6th for eligible agency personnel to decide whether or not to accept. This article reviews retirement options available for workers with at least five years of service under FERS, including whether or not they choose to take the deferred resignation offer. It is important to remember a decision to retire before September 30 will override the resignation if it is elected by next week's deadline. The time between accepting the resignation offer and September 30th will count towards FERS eligibility.

Need to discuss your federal employee benefits? Meet with an expert.

FERS Retirement Options for Federal Workforce

Important Age and Service Requirements for Federal Retirement under FERS

For federal employees with at least 5 years of service, who are below the minimum retirement age (MRA), deferred retirement is the only way to receive a pension down the road if taking the president's buyout for resignation. With 30 years of service, they can begin receiving their FERS annuity upon reaching their MRA (55 - 57). For those with 20 years with creditable FERS service start collection their pension at age 60, but there is a penalty permanently applied to the annuity (1/12 of 5% for each month under the age of 62). With at least 5 years of service, you can start receiving your FERS retirement benefit at age 62. (Click here to learn about FERS Disability retirement eligibility)

If a federal employee has reached their MRA, then they can postpone their FERS annuity with at least 10 years of service. This option allows feds to retain their FEHB plan after retiring, unlike with deferred FERS. When postponing your FERS benefit, it cannot be collected until age 62. At MRA with 30 years, 60 with 20, or 62 with 5, FERS workers are able to retire immediately. (If retiring under special provisions, read our retirement guide for LEOs, Firefighters, and ATCs,)

Need to estimate your FERS benefit amount? Try our federal pension calculator.

Accepting Trump Buyout or Not: Retirement Scenarios for FERS Employees

Depending on the amount of service, FERS employees who leave federal service have options when it comes to their pension.

Attend a three hour FERS Webinar to learn about your TSP, pension, social security, and more!

Understanding FERS Deferred Retirement and FERS Postponed Retirement

The Federal Employee Retirement System (FERS) offers various retirement options, each with its own set of rules and benefits. Learn the differences between deferred and postponed retirement under FERS, helping federal employees make informed decisions about their retirement future.

What is FERS Deferred Retirement?

Deferred retirement under FERS is an option available to federal employees who leave federal service before reaching the minimum retirement age but have accumulated at least 5 years of creditable civilian service. This retirement option allows employees to defer their retirement benefits until they reach the age of eligibility (MRA with 30 years, age 60 with 20 years, or age 62 with 5 years). Unlike immediate retirement, deferred retirement does not provide an immediate annuity; instead, it allows employees to claim their FERS annuity at a later date. As mentioned above, receiving the annuity before 62 can result in age reduction penalties.

Things to Consider Before You Apply for Deferred Retirement

To qualify for FERS deferred retirement, federal employees must leave federal employment before reaching the minimum retirement age, which varies depending on the employee's birth year. The Office of Personnel Management (OPM) oversees the application process for deferred retirement, ensuring that eligible employees receive their FERS benefits once they reach the appropriate age. It's important to note that deferred retirement does not include the FERS annuity supplement or FEHB (federal employee health benefits) eligibility, which might available to those who retire under other FERS retirement options.

Differences Between Deferred Retirement and Postponed Retirement

Deferred or Postponed Retirement: What's the Difference?

Postponed retirement under FERS is distinct type of retirement, different from deferred retirement in that it applies to federal employees who have reached the minimum retirement age and have at least 10 years of creditable service but choose to delay the receipt of their annuity until 62. Unlike deferred retirement, postponed retirement is an alternative to retiring immediately with reduced benefits. By postponing the annuity, employees avoid the reduction and receive full benefits at a later date.

Special Retirement Supplement for Social Security

With deferred retirement or postponed retirement, the FERS annuity supplement is not available. This is a significant consideration for employees who rely on the supplement as part of their retirement income. By postponing retirement, employees forfeit the supplement but may benefit from a higher annuity amount once they begin receiving their FERS pension. However, postponed retirees might be eligible to receive health insurance when they start receiving their FERS income, unlike deferred retirees. This is why postponed retirement is a better option for federal agency workers.

Key Differences: Deferred vs. Postponed Retirement

Early Retirement Options for FERS

The differences in retirement benefits between deferred and postponed retirement primarily relate to the timing and amount of the FERS annuity. Deferred retirement delays the receipt of the annuity until the employee reaches the age of eligibility, while postponed retirement allows employees to retire early but defer the annuity to 62 to avoid reductions. Both impact a federal employee's retirement plan differently, but in both cases, the retiree might need another source of income until they can claim their FERS annuity.