Maximizing Your TSP: Best Investment Strategies for the Thrift Savings Plan in 2025

The Thrift Savings Plan (TSP) is a crucial component of the retirement system for federal civilian and military personnel. As markets grow more volatile in 2025, understanding the best investment strategies for your TSP is essential to maximize your retirement savings and minimize risk. To help guide you through the intricacies of TSP planning, explore the best investment strategies in down markets, and learn how to diversify your TSP portfolio effectively. Whether you're a seasoned investor or new to the TSP, these strategies will help you make informed decisions to secure your financial future.

Check out our Free TSP Calculator to estimate your Thrift Savings Plan income in retirement.

What are the TSP Fund Descriptions and Their Performance?

Overview of TSP Fund Types

The TSP offers a range of fund types, each with its investment focus and risk profile. The G Fund invests in government securities and provides a stable return with minimal risk. The F Fund focuses on fixed-income securities, offering moderate risk and return potential. The C Fund tracks the S&P 500, providing exposure to large-cap U.S. stocks and higher potential returns. The S Fund invests in small to mid-sized U.S. companies, while the I Fund is a global international fund.

Recent and Historical TSP Returns

| Year | G Fund | F Fund | C Fund | S Fund | I Fund | |

| Inception date | 4/1/1987 | 1/29/1988 | 1/29/1988 | 5/1/2001 | 5/1/2001 | |

| 1 year | 4.49% | 5.79% | 18.36% | 11.76% | 6.42% | |

| 3 year | 4.03% | -0.36% | 12.51% | 5.91% | 5.92% | |

| 5 year | 2.87% | -0.44% | 16.81% | 11.62% | 8.34% | |

| 10 year | 2.57% | 1.64% | 12.96% | 8.97% | 5.37% | |

| Since inception | 4.65% | 5.30% | 11.16% | 9.21% | 5.18% | |

|

0.75% | 2.73% | 1.44% | -1.10% | 4.63% | |

| February | 0.36% | 2.20% | -1.30% | -5.80% | 0.91% | |

| January | 0.39% | 0.51% | 2.78% | 4.99% | 3.68% |

(Source, federal government site, tsp.gov)

Optimize Your Savings: Key Features of the TSP

To review, the TSP offers several key features that make it a valuable component of a federal employee's retirement plan. The TSP core funds include the G Fund, F Fund, C Fund, S Fund, and I Fund. Each fund has a different investment focus, ranging from government securities to international stocks. Additionally, the TSP offers Lifecycle Funds (L Funds), which automatically adjust the asset allocation of these 5 funds based on the participant's retirement timeline - although these L funds often lean too conservatively for most participants. Then, there's the Mutual Fund Window, which is another feature that allows participants to invest in a broader range of mutual funds, providing greater diversification opportunities, although it can be restrictive when it comes to cost and access.

Learn about your TSP, FERS Pension, Social Security, and more! Attend a federal retirement online workshop.

What are the Best TSP Investing Strategies for 2025?

Plan Overview: Investing Money in Your TSP and Exploring TSP Fund Options

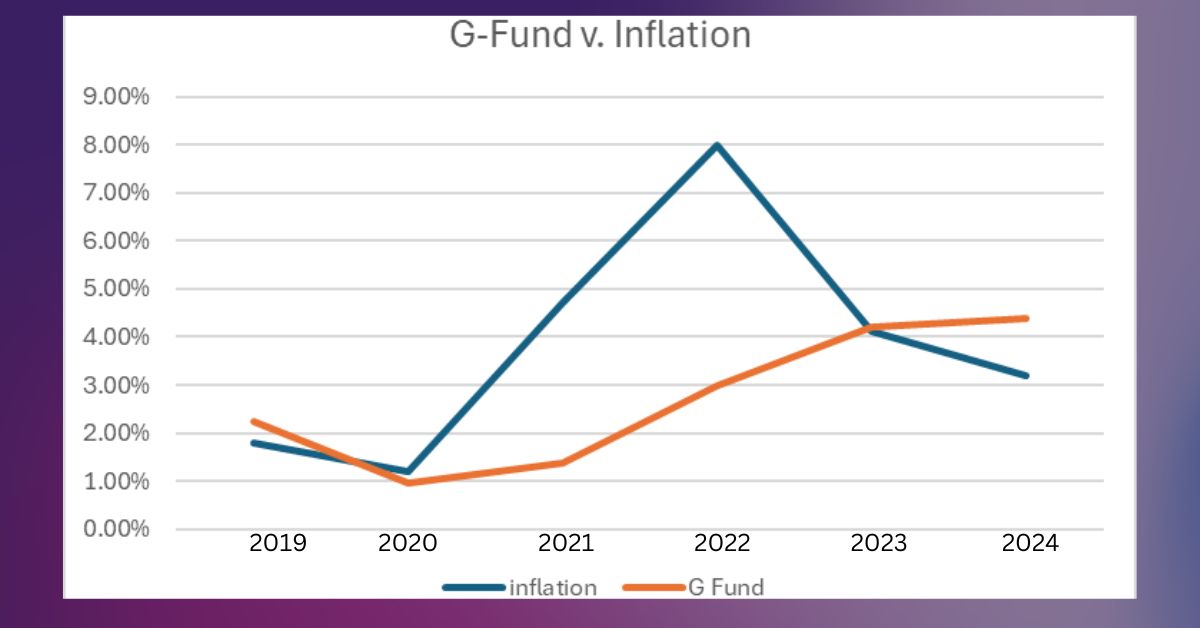

Employees should contribute as much as they can afford each paycheck to optimize government matching. Contributions are tax-deferred. When it comes to TSP investing, selecting the right allocation of investments is critical. The G Fund is considered the safest option, investing in government securities and offering a stable return, although the rate of return has not kept pace with inflation in recent years. The F Fund focuses on fixed-income securities, while the C Fund tracks the S&P 500, providing exposure to large-cap U.S. stocks. The S Fund invests in small, mid-sized, and large U.S. companies (completion index), and the I Fund offers international stock exposure. Each fund has its risk and reward profile along with relatively low fees, and understanding these can help you tailor your TSP investment strategy to align with your retirement goals. Diversifying across these funds can help balance risk and reward in your TSP portfolio. The new White House administration has disrupted markets recently with uncertain policies regarding tariffs and other aspects of the economy. Investing in the TSP if you're a federal employee in 2025 is not as cut in dry as in other years with stocks and bonds reacting to uncertain economic conditions with increased volatility, especially compared to 2024 when Thrift Savings Plan investment performance was mostly positive.

How to Choose the Right TSP Investment Strategy and Diversify Your TSP Investment Portfolio

Choosing the right TSP investment strategy involves assessing your risk tolerance, investment horizon, and retirement goals. For those with a longer time horizon, a more aggressive approach with a higher allocation to stocks, such as the C Fund or S Fund, may be appropriate. Conversely, if you're nearing retirement, a more conservative strategy with a higher allocation to the G Fund or F Fund might be prudent. It's essential to regularly review your TSP balance and adjust your asset allocation as needed to ensure it aligns with your evolving financial situation and retirement objectives. Consulting with afinancial advisor with expertise and experience with federal benefits for seeking investment advice can also provide valuable insights into optimizing your TSP investment strategy, especially in periods with higher market volatility. A financial planner can make professional asset allocation recommendations that best align with your financial situation and market conditions.

Asset Valuations: Balancing Risk and Reward in Your TSP Portfolio

Balancing risk and reward is a fundamental aspect of any investment strategy, and the TSP is no exception. While stock market returns are generally higher, providing potential to help build serious wealth, they also come with increased risk. It depends if you have time to recover before you eventually withdraw money or if you plan on withdrawing from your TSP soon (close to retirement), whether you choose to receive monthly payments, buy an annuity, or rollover/withdraw as one lump sum. On the other hand, bonds and government securities provide stability but may yield lower returns, but this risks reduced purchasing power if unable to keep pace with inflation . To achieve a balanced TSP portfolio, consider diversifying across different asset classes and TSP funds. The Lifecycle Funds (L Funds) is an option for those seeking a hands-off approach, as they automatically adjust the asset allocation based on your retirement timeline. Picking the right lifecycle fund is as easy because it is based on your retirement date, so you just need to have a rough idea of when you plan to leave federal service. By carefully balancing risk and reward, you can enhance the potential for long-term growth in your TSP, providing a comfortable retirement.

Meet with a Fed-Expert Financial Planner Today.

Strategies for Long-term Growth in TSP

Maximizing your retirement income with TSP requires focus on long-term investment goals and growth strategies, and this can be especially difficult when there is increased short-term uncertainty in the markets. One effective approach is to maintain a diversified portfolio that balances risk and reward, and a financial planner or advisor can help you reach your retirement goals. Regularly contributing to your TSP and taking advantage of any employer matching contributions can significantly enhance your retirement savings over time. Additionally, considering a mix of traditional and Roth TSP contributions can provide tax diversification, allowing for more flexibility in managing your retirement income. By staying disciplined and committed to your investment strategy, you can position yourself for long-term growth and financial security in retirement.