How Do Social Security Benefits Affect Medicare Premiums and Surcharges?

Social Security benefits can significantly impact an individual’s Medicare premiums, particularly through the Income-Related Monthly Adjustment Amount (IRMAA), which results in surcharges being added to the standard premium for Medicare Part B and Part D. As income levels rise, Medicare enrollees may face surcharges that increase their monthly premiums.

Understanding the relationship between Social Security income and Medicare premiums is crucial for retirement income planning. To manage potential surcharges, individuals can explore strategies such as minimizing taxable income from other sources, utilizing Roth conversions, or managing life-changing events that may affect their income levels and, subsequently, their Medicare costs.

Learn about FERS, Social Security, and the TSP at our Free Federal Retirement Workshops

Knowledge is Confidence!

How Does Means Testing Affect Medicare Premiums?

Means testing plays a pivotal role in determining Medicare premiums, considering an individual’s Modified Adjusted Gross Income (MAGI) to establish the cost of Medicare coverage. As income levels fluctuate, so do the premiums for Medicare Part B and potentially Part D, impacting the overall healthcare expenses for retirees.

To manage income levels and mitigate the impact of means testing on Medicare premiums, individuals can explore various strategies, such as optimizing retirement account withdrawals, considering the tax implications of IRA conversions, and proactively planning their financial activities to minimize surcharges and maintain manageable healthcare costs.

Stay on top of your federal benefits information – Subscribe to Our Newsletter

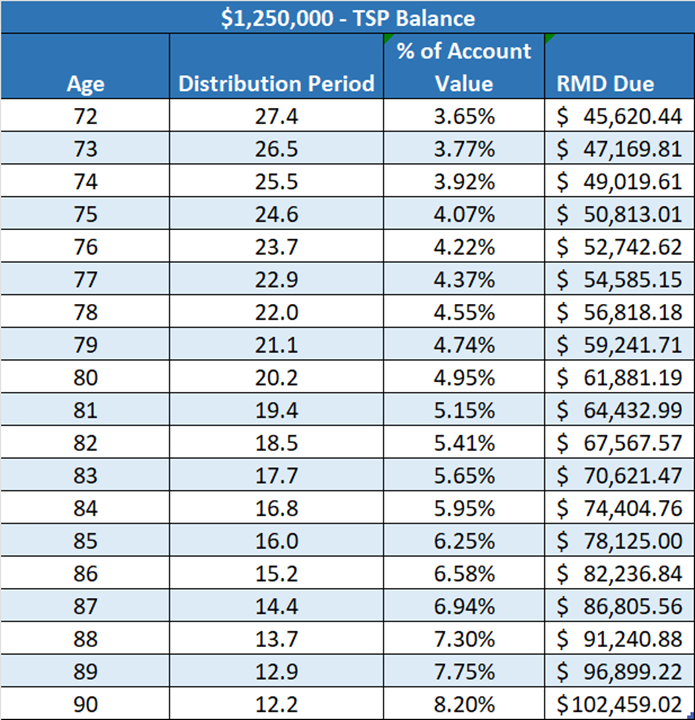

How to Calculate the RMD

The required minimum distribution for any year is the account balance as of the end of the immediately preceding calendar year divided by a distribution period from the IRS’s “Uniform Lifetime Table.” There is a different table if the sole beneficiary is the owner’s spouse who is ten or more years younger than the owner. Below is the Uniform Lifetime Table used to calculate an RMD for a single person.

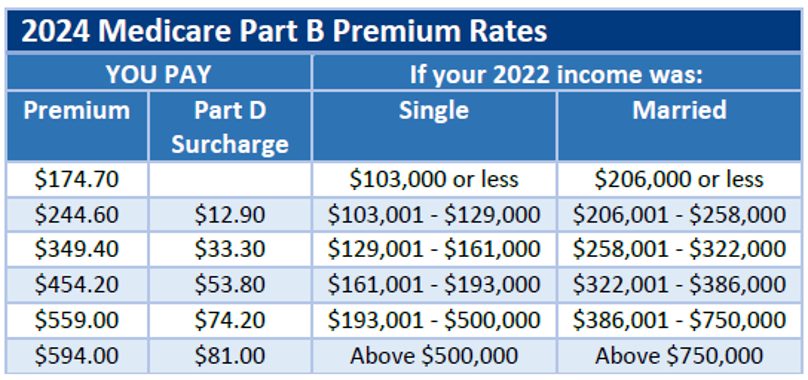

Medicare Part B & D Premiums are Based on Income

RMDs Pushing You Into Higher Medicare Part B & D Premiums

Prior to receiving RMDs, you may have been enjoying a nice retirement between Social Security, pension, and maybe a small withdrawal from the retirement account here and there. Left unchecked, the money in the traditional IRA is growing and compounding over the years. Looming in the background are RMDs that can launch you into a higher tax bracket and increase the annual cost of health insurance. Proper knowledge of how RMDs work and a plan to lower a future RMD burden can help prevent this.

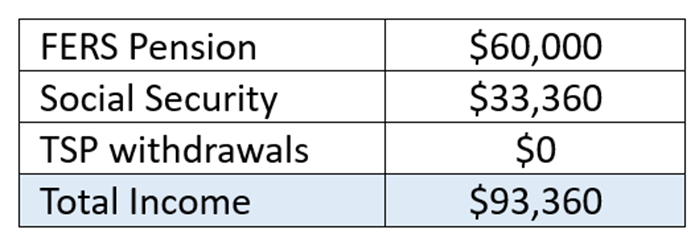

Let’s say you are a single, retired FERS annuitant and age 65. You are receiving a $5,000/month FERS pension, $2,780/month for Social Security, and taking no withdrawals from a TSP that is valued at $1,250,000.

Your total income would place you in the lowest Medicare Part B premium at $174.70/month and $0/month for Part D.

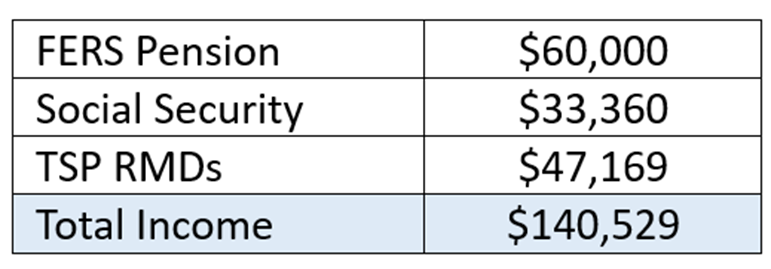

If we swap the ages from 65 to 73, the Medicare Part B premium jumps to $349.40/month for Medicare Part B and $33.30/month for Part D. That’s almost $2,500/year MORE for the same health coverage.

This is a simple explanation of how RMDs can increase health insurance in the future. The most likely scenario may be even worse. A balanced invesment strategy will generally outgrow inflation and withdrawals in the retirement account. In the previous example of the 65-year-old retiree, let’s assume the TSP is growing at a rate of 6% with no withdrawals until age 73. The account value will have grown from $1,250,000 to $1,992,310 at age 73. The RMD is much larger now.

The TSP will not stop growing if you have the funds invested and are taking no or moderate withdrawals. The compounding growth over the years will balloon the RMD down the road. Yes, Medicare income brackets will increase but usually matched with inflation. The goal of an investment strategy is to keep up with inflation and hopefully exceed inflation in the long-term. In this scenario, your Medicare Part B premium is now $454.20/month and Part D is $53.80/month which is an increase of $4,000/year.

What Can You Do?

There are some strategies to reduce health insurance premiums and taxes down the road. Conducting Roth conversions is a great way to reduce RMDs in the future as Roth IRAs do not have RMDs. Making small systematic withdrawals below higher tax brackets. If you are charitable, the use of a Qualified Charitable Distribution (QCD) will reduce income while giving to a charitable cause. There is also the Qualified Longevity Annuity Contract (QLAC) that can avoid taking RMDs until age 85.

Important!

Federal employees should take the time to understand their decision on whether to take Medicare Part B or not at age 65. If you will be falling into a premium of $349.40 or higher you may not see the financial incentive of taking Part B. Proper planning now will help you understand what your income is now and into the future which can can help you save thousands of dollars down the road.