Understanding Special Needs Trusts: Quick Reference Guide for Federal Employees and their Families

Special Needs Trusts (SNTs) provide help for individuals with disabilities who rely on government benefits. These trusts are designed to manage and protect assets for the benefit of a person with special needs, ensuring that they can maintain their eligibility for needs-based government programs such as Medicaid and Supplemental Security Income (SSI).

Special Needs Trust Information for Military and Civilian Federal Retirement Benefits

Defining a Special Needs Trust

A Special Needs Trust is a legal arrangement that allows a person with disabilities to receive income without jeopardizing their eligibility for government benefits. The trust is designed to supplement, but not replace, the beneficiary’s government benefits. By placing assets into the trust, a person with a disability can enjoy a better quality of life without risking the loss of essential support from programs like Medicaid and SSI. The trust document outlines the terms and conditions under which the trust operates, ensuring that the beneficiary's needs are met while adhering to government regulations.

Importance of a Special Needs Trust for Federal Employees

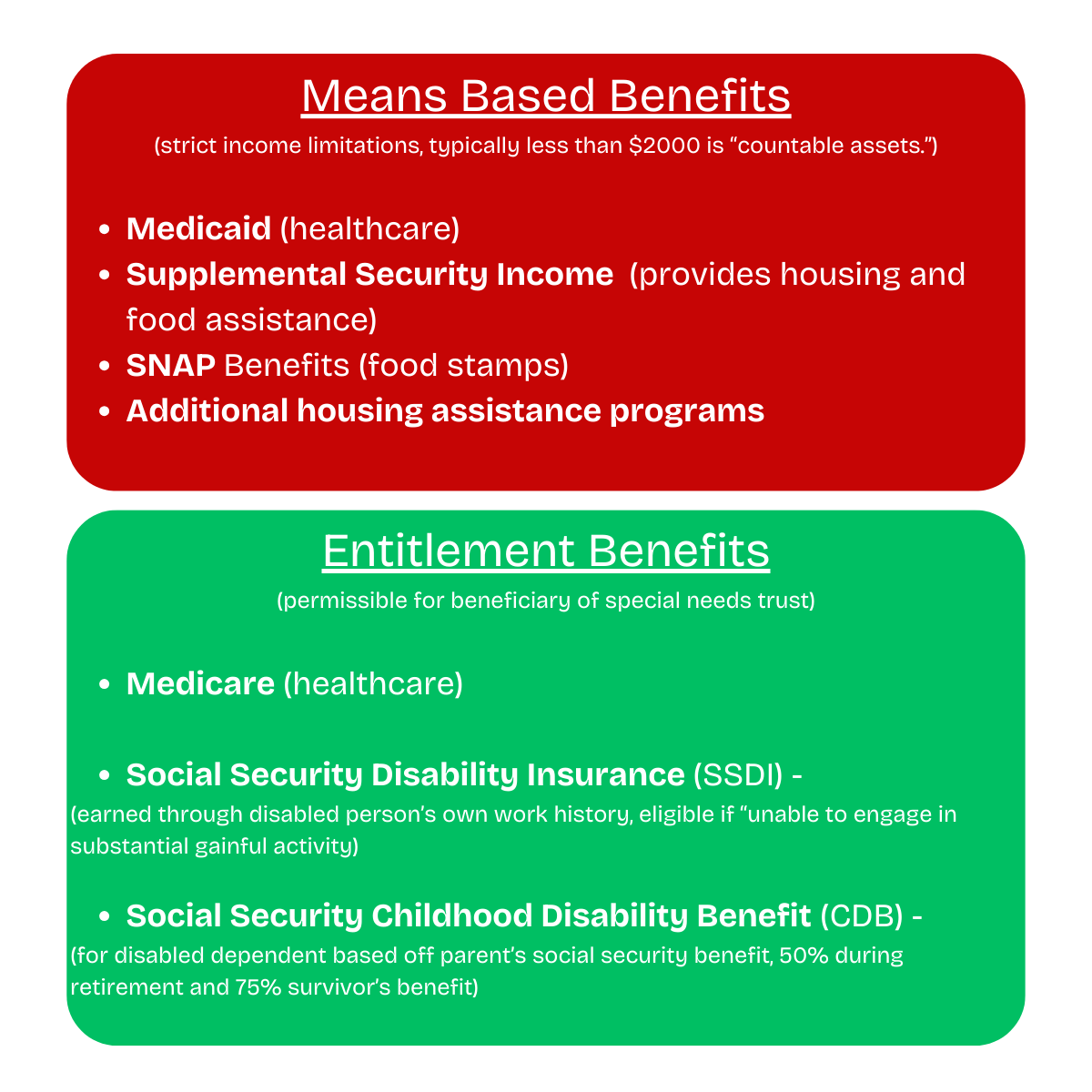

For military retirement, a survivors benefit annuity can be assigned to pay a special needs trust (SNT) directly, upon the retirees' death. For civilian federal employees retiring under FERS, a monthly amount can be paid directly to an SNT but only if retiring immediately, not with a postponed or deferred FERS retirement. The survivorship will help provide the beneficiary financial support until their death or marriage. With FERS and CSRS survivor benefits, the dependent must have experienced the disability before age 18, and before 26 to maintain health coverage under the FEHB or PSHB programs. The trust will supplement Medicaid and SSI benefits, but any FERS survivorship paid to an SNT will be offset by any childhood disability benefit (CDB) from the Social Security Administration.

Need help with your federal employee retirement benefits? Schedule a meeting.

How Does a Special Needs Trust Work?

A Special Needs Trust works by holding and managing assets for the benefit of the individual with disabilities. The trust is administered by a trustee, who is responsible for managing the trust assets and ensuring that distributions are made in accordance with the trust document. The trustee must be knowledgeable about the rules governing government benefits to avoid jeopardizing the beneficiary's eligibility. The trust can be funded with various assets, including cash, investments, and life insurance, and is designed to provide for the beneficiary's supplemental needs throughout their lifetime. Figuring out what funds are to be placed into the trust is a critical when the trust is created. An experienced estate attorney should be able to help setting up a special needs trust.

Can a Family Member Be a Trustee of SNT?

While a family member can serve as a trustee of a Special Needs Trust, it is important to consider whether they have the necessary skills and knowledge to manage the trust effectively. Family members may have a deep understanding of the beneficiary's needs, but they may lack the expertise required to navigate the complex rules governing government benefits. In such cases, it may be beneficial to appoint a co-trustee or seek the assistance of a professional trustee to ensure that the trust is administered properly.

What Are the Different Types of Special Needs Trusts?

Understanding First-Party vs. Third-Party Special Needs Trusts

There are several types of Special Needs Trusts, each designed to meet different needs. A first-party Special Needs Trust is funded with the beneficiary's own assets, such as an inheritance or personal injury settlement. Self-funded special needs trusts are often used to preserve the beneficiary's eligibility for needs-based government benefits such as Medicaid or SSI. In contrast, a third-party Special Needs Trust is funded with assets from someone other than the beneficiary, such as a parent or grandparent. This type of trust is often used in estate planning to provide for the beneficiary's supplemental needs without affecting their eligibility for government benefits.

What is a Special Needs Trust Subtrust? Exploring Pooled Trusts

Pooled Special Needs Trusts are another option for individuals with disabilities. These trusts are managed by nonprofit organizations and pool the resources of multiple beneficiaries to achieve economies of scale. Each beneficiary has a subtrust within the pooled trust, which is used to pay for their supplemental needs. Pooled Trusts can be a cost-effective option for families who may not have sufficient assets to establish a standalone trust.

Revocable vs. Irrevocable Trusts: Which is Better?

When creating a Special Needs Trust, it is important to consider whether the trust should be revocable or irrevocable. A revocable trust can be altered or terminated by the grantor, while an irrevocable trust cannot be changed once it is established, meaning determining future financial needs and medical expenses of the beneficiary is crucial. Irrevocable trusts are often preferred for Special Needs Trusts because they provide greater protection for the beneficiary's eligibility for government benefits. However, the decision between a revocable and irrevocable trust should be made in consultation with a qualified attorney who can provide guidance based on the specific circumstances of the beneficiary and their family.

How Does Estate Planning Integrate with Special Needs Trusts?

Incorporating a Special Needs Trust into Your Estate Plan

Incorporating a Special Needs Trust into your estate plan is an important step in ensuring that your loved one with disabilities is cared for after your death. The trust can be established as part of a comprehensive estate plan, which may include a will, testamentary trust, and other legal documents. By including a Special Needs Trust in your estate plan, you can ensure that your assets are used to fund the trust and provide for the beneficiary's supplemental needs without affecting their eligibility for government benefits.

Funding the Trust: What Assets Can Be Included?

Funding a Special Needs Trust involves transferring assets into the trust to provide for the beneficiary's needs. Various assets can be used to fund the trust, including cash, investments, real estate, and life insurance. It is important to work with a qualified attorney or financial advisor to determine the best assets to include in the trust and to ensure that the trust is funded in a way that maximizes the beneficiary's benefits while preserving their eligibility for government programs. Life insurance can be an effective way to fund a Special Needs Trust. By naming the trust as the beneficiary of a life insurance policy, you can ensure that the proceeds are used to provide for the beneficiary's supplemental needs after your death.

What Are the Eligibility Requirements for a Special Needs Trust?

Understanding Medicaid and SSI Rules

Eligibility for a Special Needs Trust is closely tied to the rules governing Medicaid and SSI. These programs provide essential support for individuals with disabilities, but they have strict eligibility requirements that limit the amount of income and assets a beneficiary can have. A Special Needs Trust is designed to preserve the beneficiary's eligibility for these programs by holding and managing assets in a way that does not count against the beneficiary's resource limits.

Who Can Be a Beneficiary of a Special Needs Trust?

A Special Needs Trust can be established for any individual with a disability who relies on needs-based government benefits. The beneficiary can be a child, adult, or elderly person with special needs. The trust is designed to provide for the beneficiary's supplemental needs, such as medical care, education, and personal expenses, without affecting their eligibility for government programs. It is important to work with a qualified attorney to ensure that the trust is established in compliance with all legal requirements and that the beneficiary's needs are met.