The updated 2025 TSP contribution limits are out — The Internal Revenue Code has set limits on the amount you can contribute to the Thrift Savings Plan for 2025. The regular contribution limits as increased by $500 from $23,000 to $23,500 in 2025. The catch-up limit that allows an additional contribution if over age 50 has remained the same at $7,500 for 2025.

New in 2025: Higher TSP Catch-Up Contribution Limits If You Are Ages 60, 61, 62, and 63

Beginning January 1, 2025, participants age 60, 61, 62, and 63 who are eligible for catch-up contributions will have a higher catch-up limit than the regular catch-up limit. In the years participants turn 64 and older, the catch-up limit will be the lower, regular catch-up limit amount.

Want to know how much your TSP balance will be at retirement? Check out the TSP Calculator to prepare for your retirement.

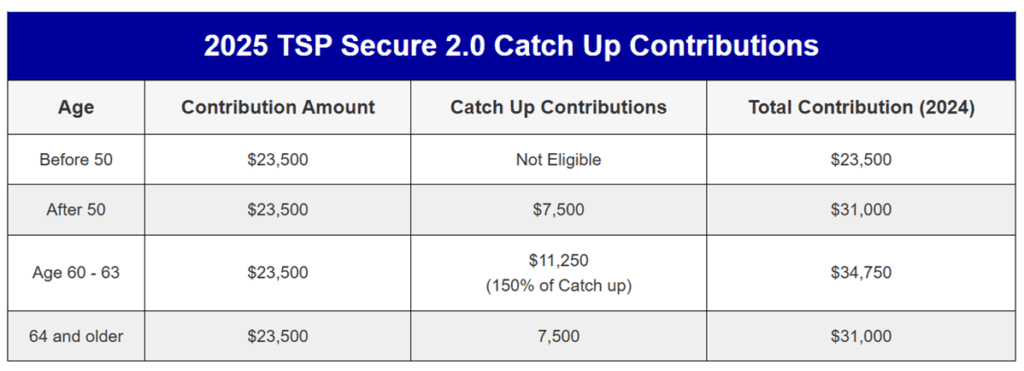

| 2025 TSP Secure 2.0 Catch Up Contributions | |||

|---|---|---|---|

| Age | Contribution Amount | Catch Up Contributions | Total Contribution (2024) |

| Before 50 | $23,500 | Not Eligible | $23,500 |

| After 50 | $23,500 | $7,500 | $31,000 |

| Age 60 - 63 | $23,500 | $11,250 (150% of Catch up) |

$34,750 |

| 64 and older | $23,500 | 7,500 | $31,000 |

SECURE Act 2.0: Supercharging Retirement Savings for Those Age 60-63

The Setting Every Community Up for Retirement Enhancement (SECURE) Act 2.0, signed into law in December 2022, is a game-changer for retirement savers. One of the most significant changes is Section 109, which significantly increases the catch-up contribution limits for those between the ages of 60 and 63. This provision aims to help older workers accelerate their retirement savings in the crucial years leading up to retirement.

New in 2025: Higher TSP Catch-Up Contribution Limits If You Are Ages 60, 61, 62, and 63

Beginning January 1, 2025, participants age 60, 61, 62, and 63 who are eligible for catch-up contributions will have a higher catch-up limit than the regular catch-up limit. In the years participants turn 64 and older, the catch-up limit will be the lower, regular catch-up limit amount.

What is the SECURE 2.0 Act?

The Setting Every Community Up for Retirement Enhancement (SECURE) Act 2.0, signed into law in December 2022, is a follow-up to the original SECURE Act of 2019. It introduces various provisions designed to enhance retirement savings opportunities for Americans.

Overview of SECURE 2.0 Act of 2022

It aims to make it easier for individuals to save for retirement and to encourage employers to offer retirement plans. The act encompasses a wide range of changes to retirement savings rules, including:

Key Provisions:

- Secure 2.0 Catch Up Contributions: Raises the catch-up contribution limit for individuals aged 60-63, allowing them to contribute more to their retirement accounts in the calendar year leading up to retirement.

- Required Minimum Distribution (RMD) Age Increase: Pushes back the age at which RMDs must begin from 72 to 73 in 2023, and eventually to 75 by 2033.

- Automatic Enrollment in 401(k) Plans: Requires new 401(k) and 403(b) plans to automatically enroll eligible employees, with the option for employees to opt out.

- Student Loan Matching: Allows employers to make matching contributions to retirement plans based on an employee’s student loan payments.

- Part-Time Worker Eligibility: Expands eligibility for 401(k) plans to part-time workers who have completed at least 500 hours of service for two consecutive years.

- Emergency Savings Accounts: Permits employers to offer emergency savings accounts linked to retirement plans, providing employees with a way to save for unexpected expenses.

Check out our article on SECURE 2.0

Knowledge is Confidence!

Understanding Catch-Up Contributions

Catch-up contributions allow participants aged 50 or older to contribute more to their retirement plans than younger savers. This is designed to help them compensate for years when they may not have been able to save as much. Currently, anyone aged 50 or over can contribute an additional $7,500 beyond the standard elective deferral limit of $22,500 in 2024, bringing the total to $30,000.

The SECURE Act 2.0 Boost: How Does the Age 60-63 Catch-Up Contribution Work?

Starting January 1, 2025, catch up contributions SECURE Act 2.0, Section 109, dramatically increases the dollar limit for those aged 60 to 63. In 2025, this group could contribute an additional $11,250 (higher catch-up limit, up to 150% of the regular catch-up limit) on top of the current standard $22,500, totaling $33,750.

And that’s not all. The increased catch-up limits will be indexed for inflation after 2025, meaning they’ll keep pace with the rising cost of living, ensuring that the value of these contributions isn’t eroded over time.

Roth Catch Up SECURE 2.0 Contributions

Secure Act 2.0 Roth catch up contributions are the other major change. Starting in 2026, if your income is above $145,000, your catch up contributions need to be in the Roth TSP or Roth 401k. The ability to reduce your current year’s income would be gone, but the process will still grow tax-deferred and potentially be tax-free at distribution. The tax treatment may be different, but Secure 2.0 Roth Catch up amounts are the same as the above chart.

Who Benefits Most?

This change is particularly advantageous for those who may have started saving for retirement later in life, or for those who wish to take advantage of the tax benefits of contributing more to their retirement accounts in their peak earning years. It’s also a boon for those who simply want to boost their retirement savings as much as possible in the years leading up to retirement.

- Part-time workers: The act expands eligibility for 401(k) plan participation to part-time workers who have completed at least 500 hours of service for two consecutive years, providing them with more opportunities to save for retirement.

- Employees with student loans: Employers may now offer matching contributions to retirement plans based on employees’ student loan payments, helping them balance debt repayment with retirement savings.

What This Means for Employers

Employers will need to be prepared to implement these new catch-up contribution limits. They should update their payroll systems and inform their employees about the increased limits. It’s also a good opportunity for employers to review their retirement plan offerings and ensure they are meeting the needs of their employees, particularly those in the 60-63 age bracket.

The Bigger Picture

The SECURE Act 2.0 represents a significant step forward in helping Americans save for retirement. By increasing catch-up contribution limits for those in their 60s, it provides a valuable tool for older workers to secure their financial future. As this new provision takes effect in 2025, it’s expected to have a positive impact on retirement savings rates and overall retirement readiness among this age group.

The enhanced catch-up contributions under SECURE Act 2.0 offer a unique opportunity for those aged 60 to 63 to supercharge their retirement savings. By taking advantage of these higher limits, individuals can make significant strides towards a more comfortable and secure retirement.

Reach Out to Us!

If you have additional federal benefit questions, contact our team of CERTIFIED FINANCIAL PLANNER™ (CFP®) and Chartered Federal Employee Benefits Consultants (ChFEBC℠). At PlanWell, we are federal employee financial advisors with a focus on retirement planning. Learn more about our process designed for the career fed.

Preparing for federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out, and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.