Exploring the Benefits of a Roth IRA Conversion: Key Considerations and Tips

Roth conversions have become an important topic of conversation with our clients. There are several reasons for this:

- Cheaper cost on the conversion when investments are down (fewer taxes owed)

- Anticipation of taxes going up

- RMDs pushing you into a higher tax bracket (watch out for the RMD trap)

- Tax-free growth

What is a Roth Conversion?

A Roth IRA conversion is a strategy that transfers traditional retirement funds into a Roth IRA. You pay taxes on the money converted now, but the funds in the Roth IRA will grow tax-free and avoid RMDs. Taking advantage of market downturns can make Roth conversions even more appealing.

Tax Savings During Down Markets:

When the market is down like 2022, you are receiving a discount on your Roth conversion. For example, let’s say you held the S&P 500. The S&P 500 was down -18.17% in 2022.

- S&P 500 purchased on 1-1-2022

- Cost-basis = $100,000

- 1,000 shares bought

- Value on 1-1-2023 = $81,830 (still have 1,000 shares)

If we convert the 1,000 shares based on a value of $100,000:

- Federal tax at 32% = $32,000

- State tax at 5% = $5,000

- Total taxes owed = $37,000

Convert the same 1,000 shares based on $81,830:

- Federal tax at 32% = $26,185

- State tax at 5% = $4,091

- Total taxes owed = $30,276

Discount on taxes owed = $6,724

The tax savings could be even more significant if you choose more beaten-up investment classes. The strategy to do this would involve converting shares of the investment into a Roth IRA. Also, any additional gains within the Roth IRA will enjoy tax-free growth.

Save Taxes Before They Increase:

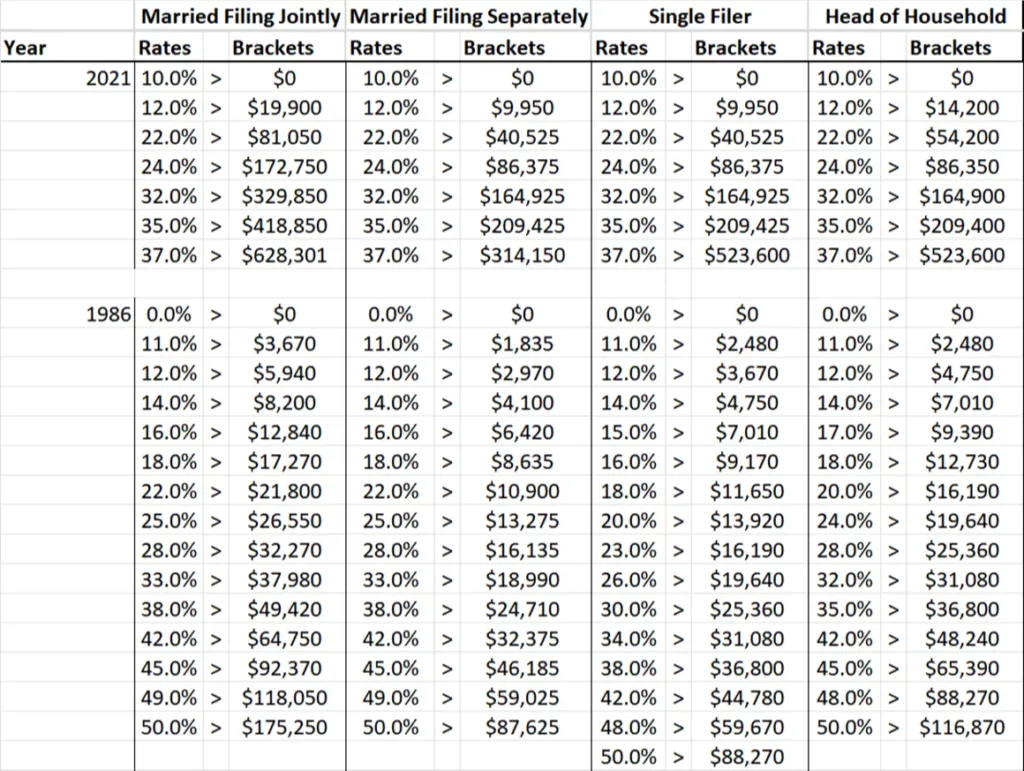

Most of our clients believe they will be in a lower tax bracket in retirement, however, it comes as a surprise when we explain they will most likely be in the same tax bracket or even higher (due to RMDs). The current tax laws will sunset in 2025, and projections show that taxes will most likely increase. Historically, the current tax laws are the lowest they have ever been. If you believe taxes will be higher in the future, it could make sense to pay the taxes now at a lower bracket through a Roth conversion. The table below illustrates the stark differences in the current tax laws and the tax laws in 1986. If you filed a joint tax return and made over $64,750 ($193,000 in today’s dollars), then you would be in the 42% tax bracket! That is an 18% increase from today’s tax rates.

*$64,750 inflation-adjusted to present value (3% inflation rate) is equivalent to $193,000 in today’s dollars

RMDs Can Push You Into a Higher Tax Bracket

Another reason to conduct Roth conversioans is to avoid being pushed into a higher tax bracket once you reach RMD age. If you have substantial pre-tax assets, the RMDs could be very large, and a surprise comes tax time. Converting the pre-tax assets into a Roth IRA will lower the RMD burden. In addition, Roth IRAs are not required to take RMDs, so you can lower your taxes and enjoy tax-free growth in the Roth IRA.

Summary:

If you have pre-tax retirement assets, you should consider conducting Roth conversions this year. In our opinion, it makes the most sense to do this only if you can afford to pay the taxes owed with cash out of pocket. It is not as advantageous to pay the taxes owed on a Roth conversion out of the traditional account. Down markets provide additional incentives to take advantage of Roth conversions, so try to look for asset classes with the lowest return in your portfolio, but you believe still offer potential, long-term growth.

Another great option is utilizing a Roth 401(k) or Roth TSP. If you haven’t checked out our article on securing your financial future with a Roth 401(k), take a look to understand how these accounts might benefit you.

Reach Out to Us!

If you have additional federal benefit questions, reach out to our team of CERTIFIED FINANCIAL PLANNER™ (CFP®) and Chartered Federal Employee Benefits Consultants (ChFEBC℠). Our advisors also hold their AIF designation. At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars through our online workshop page. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Interested in having PlanWell host a federal retirement seminar for your agency? Reach out, and we can collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting with our team.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.