Net Unrealized Appreciation (NUA) is a valuable tax strategy that can significantly impact your financial future. Whether you’re a long-time investor or you’re just starting to explore your options, understanding NUA can be a game-changer. In this article, we’ll break down the concept of NUA, explaining what it is, how it works, and why it matters for your financial planning.

What is Net Unrealized Appreciation (NUA)?

Net unrealized appreciation (NUA) is the difference between the original cost basis of an asset and its current market value. It is most commonly used in reference to employer stock held in a tax-deferred retirement account, such as a 401(k) plan. When you contribute to such plans, your contributions grow over time, and the company stock may appreciate. NUA comes into play when you want to distribute assets from your retirement plan.

Why Does NUA Matter?

NUA can provide several advantages:

Tax Efficiency: By paying tax only on the cost basis of the employer stock initially, you can potentially save on taxes. This strategy can be especially beneficial if your employer’s stock has significantly appreciated. Learn more about tax strategy for federal employees.

Estate Planning: NUA can also play a role in estate planning, potentially allowing your heirs to inherit the stock at a stepped-up cost basis, potentially reducing their tax liability.

How Does NUA Work?

Eligibility: To take advantage of NUA, you must be eligible. Typically, this means you must be at least 59½ years old, no longer employed by the company, or have experienced a qualifying event such as disability or death.

Distributing Employer Stock: Instead of rolling over your entire retirement plan into an Individual Retirement Account (IRA), you decide to distribute the employer stock in-kind. This means you take possession of the actual shares of company stock.

Taxation: When you distribute the employer stock, you’ll pay income tax only on the cost basis of the stock, not on the entire value of the distribution. The difference between the cost basis and the current market value of the stock is considered NUA.

Deferred Tax on NUA: You defer the tax on the NUA until you decide to sell the stock. When you eventually sell the stock, you’ll pay long-term capital gains tax on the NUA, which may be lower than your ordinary income tax rate.

Drawback of NUA

The main drawback of NUA is the initial tax from the lump sum withdrawal of the cost basis on the company stock. Depending on the amount, it may reflect a high overall tax bill for the withdrawal year.

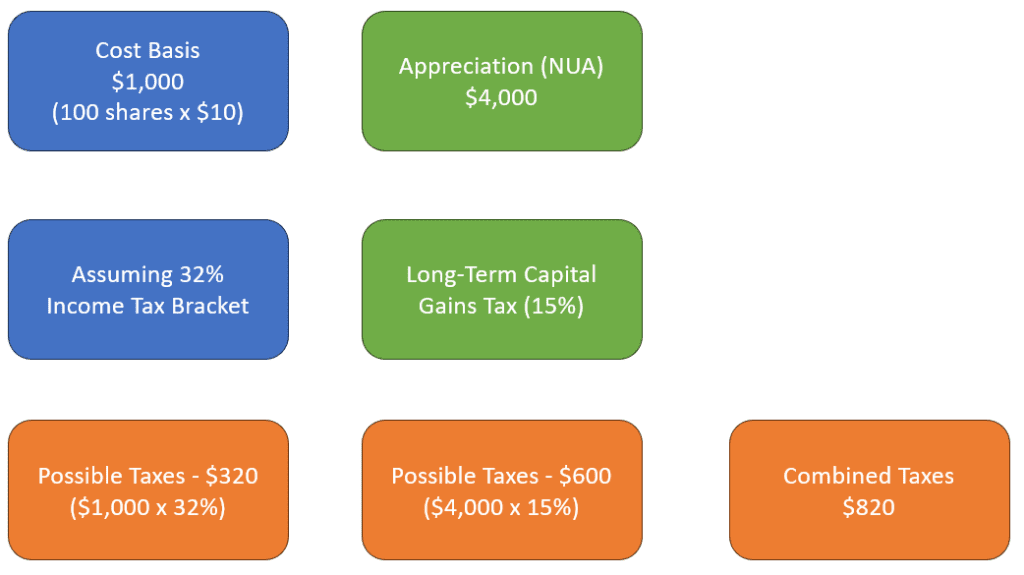

Example of How NUA Works

Let’s say you have 100 shares of employer stock in your 401(k) plan. You bought the stock at $10 per share, so your cost basis is $1,000. The current market value of the stock is $50 per share.

If you take a distribution of your employer stock from your retirement account, you will increase your income by the cost basis of the stock, or $1,000. You can avoid paying taxes based on the appreciation of the stock, which is NUA.

Immediately after you distribute the stocks, you sell all the shares to generate cash. Your may have a combined tax bill of $820. $320 from the basis and $600 from capital appreciation

Compare that to a distribution from a retirement account. If you roll over the same company stock to an IRA, the entire amount will be considered income tax when you distribute. The tax liability may be $1,600.

Lastly, if you decide to hold on to the stock and not sell it immediately, any appreciation of the stock from that point on may be treated as short-term or long-term gains, depending on how long you’ve held it.

Conclusion

Net Unrealized Appreciation is a powerful tool to enhance your retirement planning and investment strategy. By understanding NUA, you can make informed decisions about your retirement account distributions, tax implications, and investment diversification. Before implementing any NUA strategy, it’s crucial to consult with a tax professional to ensure it aligns with your specific financial goals and circumstances. NUA is not a one-size-fits-all solution, but when used effectively, it can provide significant financial benefits.

If you have Ristricted Stock Options (RSUs), you can learn more about it in our article Restricted Stock Units (RSU): Everything You Need to Know

Reach Out to Us!

If you have additional federal benefit questions, contact our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciaries (AIF®). At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars federal retirement webinars. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out, and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting contact us.

About David Fei

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

David has been in the financial services industry for over 20 years, bringing a wide range of experience in personal finance to every client relationship. He specializes in helping federal families tackle life's biggest financial challenges—retirement income planning, educational funding, and investment strategy. David's approach is grounded in education. He believes that when clients truly understand their options, they make better decisions. That's why he takes the time to explain the "why" behind every recommendation.