With the New Year comes new resolutions. Before starting any new gym memberships or changing your diet, you may want to ensure that your financial health is in order. This means updating your 401k or retirement plan contribution amounts and making sure that your investments are suit for your goals. Here are some of the key planning numb you should pay attention to.

Retirement

For those of us who have an employer sponsor plan (401k, 403b, or the Thrift Savings Plan (TSP)), the annual contribution has been increased to $22,500 for 2023. If you are over the age of 50, the catch-up contribution has been increased to $7,500. You should consider maximizing your retirement plan contribution and spread it out over the year.

IRA contribution has been increased to $6,500 with the same $1,000 catch-up if you are over 50. The key is to know that 401k and IRA contribution are separate, that means you could contribute to an employer sponsored plan like a 401k and into an IRA.

While anyone can contribute to a Traditional IRA, the key is to understand if the contribution is deductible based on your income. The Roth IRA is quite different in the fact that contributions are subject to an income limit. You are only eligible to make a full Roth contribution if your MAGI (Modified Adjusted Gross Income) is below $138,000 for a single filer, and $218,000 for married couples filing jointly

If you are self-employed, I will encourage you to speak to your accountant regarding your contribution amount. The maximum amount for 2023 is $66,000 for defined contribution plans.

Taxes

The social security wage base jumped to $160,200, so higher income earners will see their social security tax go up.

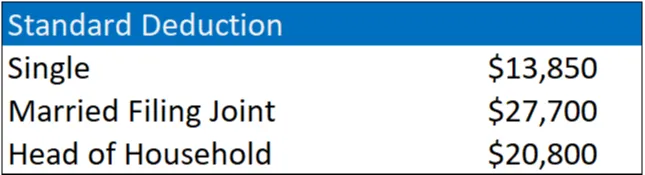

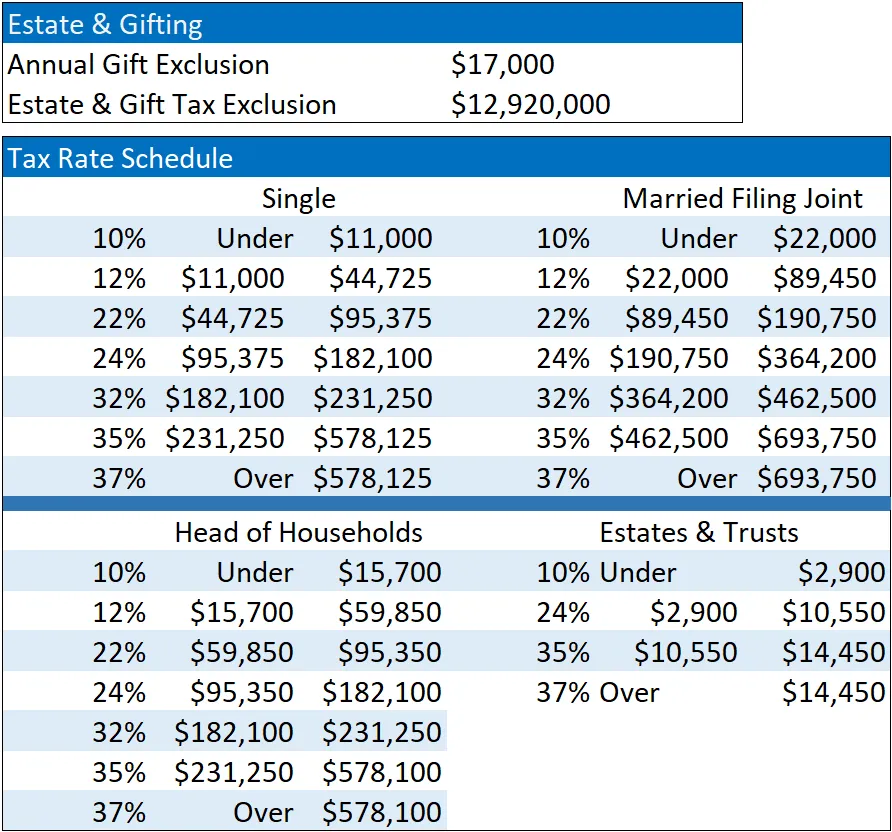

The standard deduction for single filers has increased to $13,850 and $27,700 for married couples filing together. While the tax brackets have remained the same, it is essential to note that bracket limits have been adjusted for inflation. Lastly, the annual gifting exclusion has been increased to $17,000, while the estate/gift tax exclusion is now $12,920,000.

Retirees

Social Security had a 8.7% cost of living increase! That is the most significant change since 1981. On top of that, Medicare Part B Premium had a slight reduction. Both are great for retirees.

The Required Minimum Distribution (RMD) has been changed to age 73 for 2023. So, that means you are required to start taking distributions from your IRA, or if you are retired, from your 401k in 2023. If you are still working, you could avoid taking RMD from your current employer’s 401k. However, you are still required to take RMDs from IRAs and former employer’s 401k plans.

If 2023 is the first year you are taking RMDs, you can delay your 2023 distribution until April 1st of 2024 without incurring a penalty. However, keep in mind that you will need to take two RMDs in 2024 (the delayed 2023 distribution and the 2024 distribution by 12/31/2024). Please reach out to us or speak to your accountant if you need assistance deciding if delaying the first RMD is a good decision.

Health Savings Account

If you have a high deductible health plan, you need to contribute to the Health Savings Account (HSA). Unlike Flexible Spending Accounts, balance in the HSA does not expire, and it will rollover year over year. The biggest advantage of the HSA is the ability to invest the funds and grow it tax deferred. It is one of the biggest overlooked planning tool available.

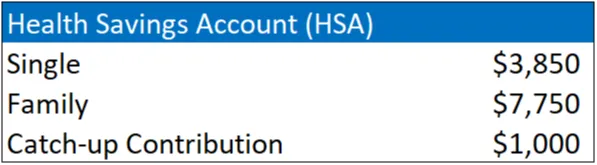

You can contribute up to $3,850 for single filers and $7,750 for the family. If you are over age 50, you can make an additional contribution of $1,000.

Reach Out to Us!

If you have additional federal benefit questions, reach out to our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciary (AIF®). At PlanWell, we focus on financial planner for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars through our online workshops. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting through our contact page.