Oversight of the Thrift Savings Plan: How Safe is the TSP?

As a defined contribution plan, the TSP offers a range of investment options and benefits tailored to the unique needs of federal employees, but the biggest retirement plan in the world might have less oversight and protections than one would assume. This article will look at potential problems with the Thrift Savings Plan, including legislative issues, oversight concerns, and then we'll examine how the current White House could exasperate these weaknesses.

Check out our TSP Calculator to estimate your retirement income.

How Safe are Your Retirement Savings in the TSP?

Security Measures in Place for TSP Accounts

The security of TSP accounts is a top priority for the Federal Retirement Thrift Investment Board (FRTIB), which oversees the plan. The TSP employs a range of security measures to protect participants' retirement savings and account information. These include robust cybersecurity protocols, multi-factor authentication for account access, and regular audits to identify and address potential vulnerabilities. The FRTIB continuously monitors the security landscape to adapt and enhance its protective measures, ensuring that TSP participants can have confidence in the safety of their retirement savings. However, unlike similar 401(k) and 403(b) plans, the Thrift Savings Plan's governing body is the FRTIB and they are not required to comply with ERISA (Employee Retirement Income Security Act).

Comparing TSP with 401(k) and Other Retirement Plans

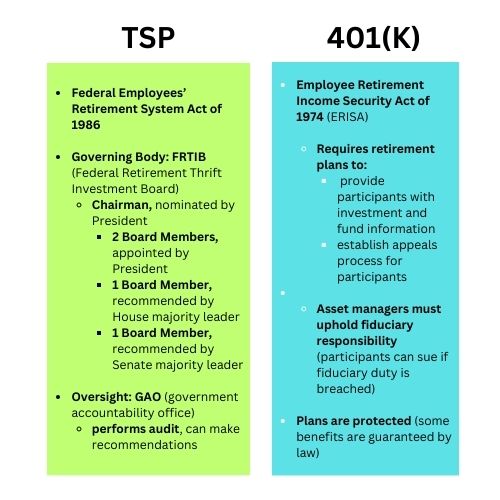

The Thrift Savings Plan shares many similarities with 401(k) plans, but there are also key differences that set it apart. In terms of rules and regulations established by Congress, the TSP was established by the Federal Employees' Retirement System Act of 1986 and not the 1974 law. ERISA requires plans to provide participants with plan information, including important facts about plan features and funding. It also establishes fiduciary responsibilities for those who manage and control plan assets, requires plans to establish a grievance and appeals process for participants to get benefits from their plans, and gives participants the right to sue for benefits and breaches of fiduciary duty. Essentially, ERISA is designed to ensure that employees receive the retirement and health benefits they were promised by their employers. The TSP, on the other hand, follows rules decided by the Federal Retirement Thrift Investment Board (FRTIB).

Role of the Federal Retirement Thrift Investment Board (FRTIB)

The Federal Retirement Thrift Investment Board plays a crucial role in the administration and oversight of the Thrift Savings Plan. As an independent government agency, the FRTIB is responsible for managing the TSP's assets, ensuring compliance with federal regulations, and safeguarding the interests of plan participants. The board's fiduciary duty mandates that it acts solely in the best interest of TSP participants, prioritizing the security and growth of their retirement savings. The FRTIB's governance structure and commitment to transparency further bolster the trust and reliability of the TSP system, but the 5 member board has the final say when it comes to investment options, modernization, and other aspects of retirement investing that ERISA provides for private sector plans like 401(k)s.

GAO Audits of TSP and President's Influence

While the Government Accountability Office (GAO) conducts regular audits of the TSP and makes recommendations, the board is under no legal obligation to follow these suggestions. The last audit took place in August 2024 and noted some vulnerabilities with the plan's new recordkeeping system that launched in 2022 along with the new TSP Mutual Fund Window, mobile app, and new TSP website for account access. The FRTIB is comprised of five members, including two who are directly appointed by the White House and another one, the Chairman, who is chosen by Presidential nomination and must be approved by the Senate. The other two are appointed by recommendations from the Speaker of the House and the Senate majority leader.

The TSP in Trump's 2nd Term

General Market Uncertainty: Understanding the Risks

TSP participants should be aware of the inherent risks associated with investing in the Thrift Savings Plan and know their risk tolerance. Market volatility can impact the value of TSP funds, particularly those invested in stocks and bonds. While this is always the case when investing, it is unclear how the markets will behave under the new administration. It is unclear what impact tariffs could have on investments in the TSP, either good or bad. What can be said is that the President's actions will disrupt markets on some level and this may create an environment of increased volatility.

Need help with your investment plan? Meet with a Fiduciary Financial Advisor for Federal Employees.

Future of FRTIB Board Members

The board members on the FRTIB cannot be fired unless there's been gross misconduct, such as negligence of duty, that has proven. There is a formal process held for removal. That being said, the four-year terms for two members are up in 2025 and the chairman's term expires in 2026. Whether picked directly by the president or the GOP leaders in Congress, who Trump wants to sit on the board could significantly impact the federal government's and military's retirement savings plan, which holds over 895 billion dollars in assets. After the President's attempt to fire at least a dozen inspector generals in his first week of office, it is clear there will be a hostile relationship between the executive branch and government watchdogs, meaning the GAO can expect difficulty in maintaining proper oversight of the federal employee retirement savings plan.

The Debt Ceiling and the G-Fund

When Congress doesn't lift the debt ceiling for the US to pay its obligations, "extraordinary measures" can be taken by the Treasury Department to prevent default, including borrowing money from the G Fund as the government needs. While this admittedly has never caused a direct loss for any TSP investor, it still makes many civilian feds and those in the uniformed services uneasy when the government lends cash out directly from the funds they use to save for retirement income. During the first Trump presidency, the Treasury Department had to take these measures on three occasions: twice in 2017 and once in the summer of 2019. Obviously, it remains unknown whether this will reoccur, but is an aspect of the TSP's G Fund that federal agency and defense workers should be aware of.

More TSP Information for Federal Workforce

Withdrawing Money from the TSP

TSP participants have several withdrawal options available to them, allowing for flexibility in accessing their retirement savings. These options include partial withdrawals, full withdrawals, and installment payments. Upon retirement, participants can choose to receive their withdrawals as a single lump sum, a series of monthly payments, or a combination of both. The TSP also offers the option to transfer funds to an Individual Retirement Account (IRA) or another eligible retirement plan, providing additional flexibility in managing retirement income. Understanding these options, and potential penalties based on age, is crucial for participants to effectively plan their retirement income strategy.

Close to retiring from the federal government? Attend a Free Federal Retirement Online Workshop

Advantages of the TSP for Federal Employees

The Thrift Savings Plan offers several advantages that make it an attractive option for federal employees. Its low-cost structure ensures that more of participants' contributions are invested, maximizing the growth potential of their retirement savings. The TSP's automatic enrollment and matching contributions for FERS employees provide a strong foundation for building retirement wealth. Additionally, the TSP's diverse investment options and portability make it a flexible and adaptable choice for federal employees at all stages of their careers. These advantages, combined with the plan's robust security measures, make the TSP a valuable component of the federal retirement savings system. Having a TSP Planner on your side can give your financial plan an even greater advantage.

Potential Drawbacks of the TSP

Despite its many benefits, the Thrift Savings Plan is not without its drawbacks. Other than the concerns detailed above, one potential limitation is the relatively limited range of investment options compared to some private sector retirement plans. This may restrict participants' ability to fully diversify their portfolios or pursue specific investment strategies. Additionally, the TSP's withdrawal rules and RMD requirements can be complex and may pose challenges for some participants. Finally, while the TSP's low-cost structure is a significant advantage, it may also result in fewer resources for personalized financial advice and support. Participants should carefully consider these factors when evaluating the TSP as part of their overall retirement strategy.