Complete Guide to the Federal Employee Retirement System

The following information is meant to be an exhaustive explanation of the FERS pension. The intention is to be a single resource when preparing for a federal retirement. The article is lengthy, we suggest reviewing our FERS page for a short summary. To easily reference a piece of information, use the dropdown on the table of contents. The following is covered:

- Pension Calculations

- Costs

- RSCD vs LSCD

- Eligibility and When to Retire

- Minimum Retirement Age (MRA)

- High-3 Calculation

- Determining Creditable Service

- Military Buy-Back

- Unused Sick Leave Conversion

- Alternative Retirement Options

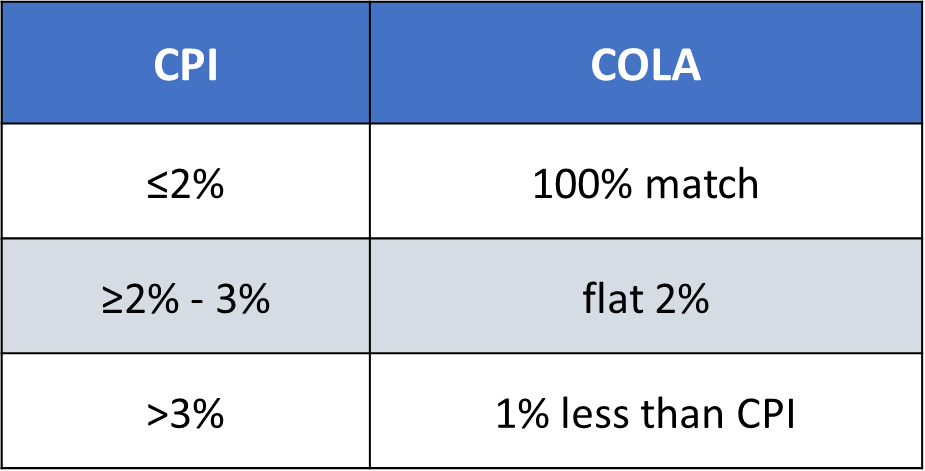

- COLAs

- Post-Retirement Options

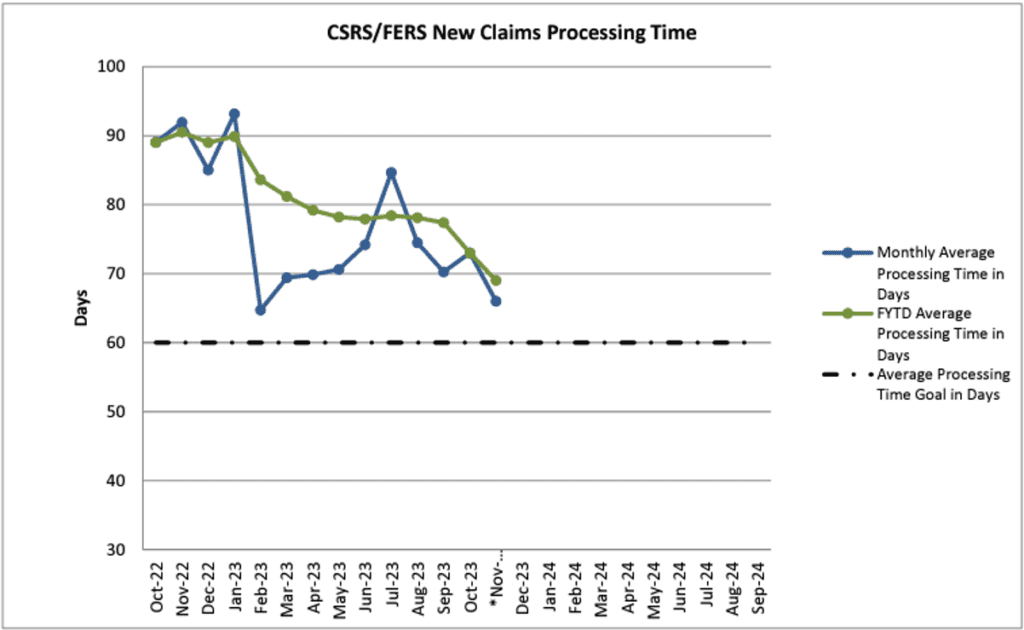

- OPM Backlogs

- Best Dates to Retire

Table of Contents

FERS – Three Main Components

Congress created the Federal Employees Retirement System (FERS) in 1986, and it became effective on January 1, 1987.

The Federal Employees Retirement System (FERS) is a retirement plan for federal employees in the United States. It was established in 1987 to replace the older Civil Service Retirement System (CSRS). FERS is a three-tiered system that includes the following components:

Basic Benefit Plan (Pension): Similar to the traditional pension plan, federal employees under FERS receive a defined benefit based on their years of service, high-3 salary, and a multiplier formula. This portion provides a guaranteed monthly annuity upon retirement for life.

Thrift Savings Plan (TSP): The TSP is a defined contribution plan that allows federal employees to contribute to a tax-advantaged retirement account. The Federal Government contributes an automatic 1% and up to 4% of your basic pay depending on contributions made. Employees can choose how to invest their TSP contributions among various investment funds.

Social Security: FERS employees also participate in the Social Security system, with deductions made from their salary. Social Security benefits are provided based on the individual’s earnings and work history.

FERS aims to provide federal employees with a comprehensive retirement package that includes a guaranteed pension, personal savings through TSP, and Social Security benefits. The combination of these three components is designed to provide a secure income stream for retirees. We will focus on covering the FERS basic benefit plan, also known as the FERS pension.

FERS is Not Created Equally for Everyone

If you entered service after 2014 you are paying 450% MORE into the same system. New FERS employees are paying 4.4% for the same exact pension that at one time only cost 0.8%. In total new FERS employees are having 12.05% deducted from their paychecks right off the top for legacy retirement systems.

FERS = Federal Employees’ Retirement System

FERS-RAE = Revised Annuity Employees

FERS-FRAE = Further Revised Annuity Employees

FERS

- Entered service between 1/1/1987 – 12/31/2012

- 0.8% to FERS

FERS-RAE

- Entered service between 1/1/2013 – 12/31/2013

- 3.1% to FERS

FERS-FRAE

- Entered service between 1/1/2014 – Current

- 4.4% to FERS

Total Amount of Deductions for FERS Employees

Employees are required to pay into FERS, Social Security and Medicare. The employer also contributes 6.2% for Social Security and 1.45% for Medicare separately.

FERS

- 0.8% to FERS

- 6.2% to Social Security

- 1.45% to Medicare

- Total = 8.45%

FERS-RAE

- 3.1% to FERS

- 6.2% to Social Security

- 1.45% to Medicare

- Total = 10.75%

FERS-FRAE

- 4.4% to FERS

- 6.2% to Social Security

- 1.45% to Medicare

- Total = 12.05%

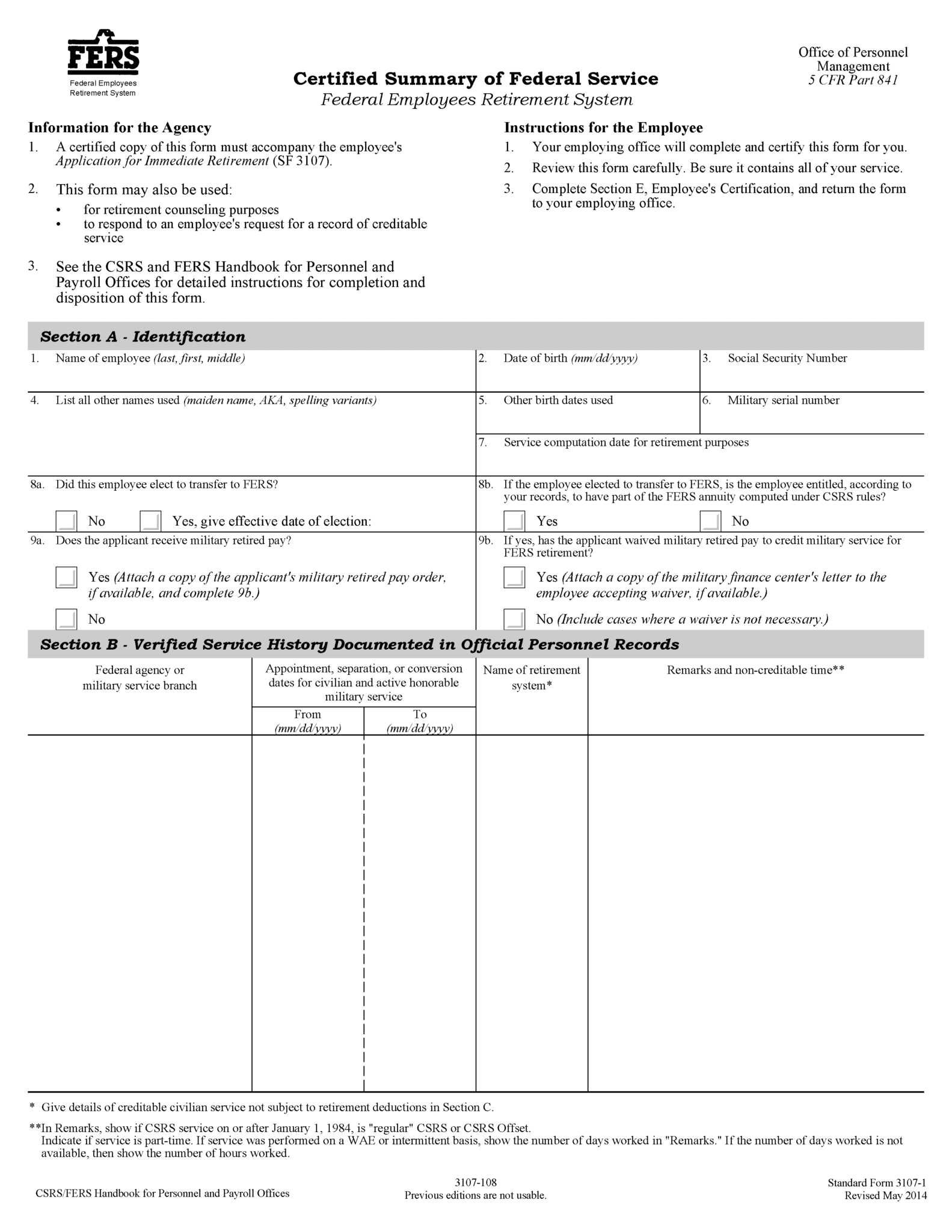

Confirm Your Retirement Service Computation Date (RSCD)

RSCD is NOT Leave Service Computation Date (LSCD)

The RSCD is used to calculate your federal years of service for the pension calculation. It is important to not confuse the RSCD with the LSCD date that is on your leave and earnings (LES) statement. Often, the LSCD and RSCD are the same, however it is better to assume they are not. Primary reasons for having a different RSCD and LSCD include:

- Breaks in service

- Military time

- Entered service with higher per-pay-period leave

At retirement, OPM will review all of your SF-50’s to confirm the RSCD after you file retirement paperwork. You can verify your creditable service time by submitting an SF-3107 – go to page 9 of the form titled, “Certified Summary of Creditable Service.” You can submit to HR to verify the RSCD. We recommend confirming the RSCD sooner than later to avoid any surprises come retirement.

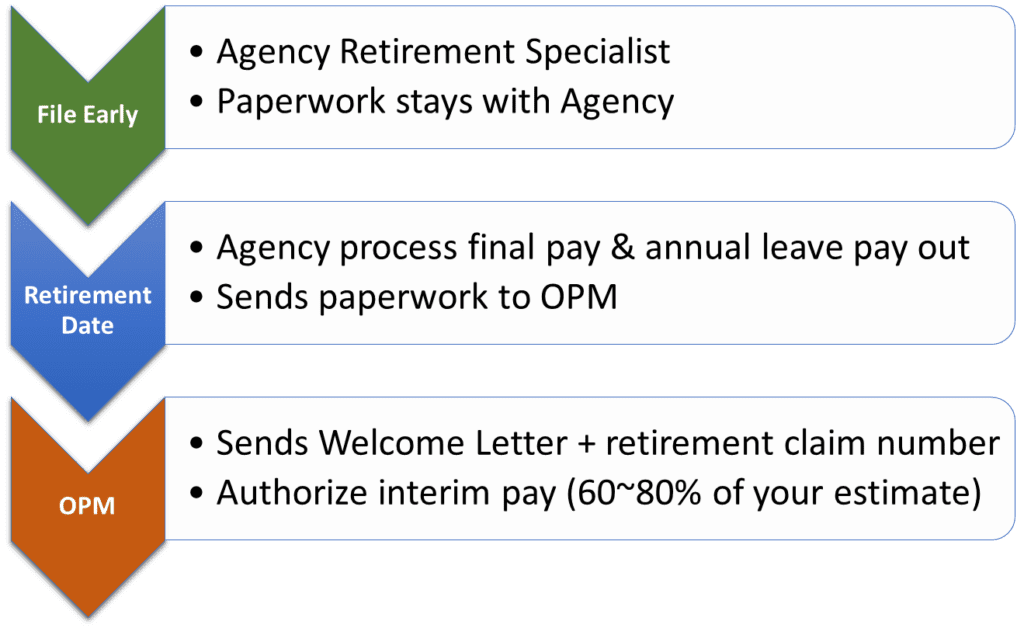

How to Retire

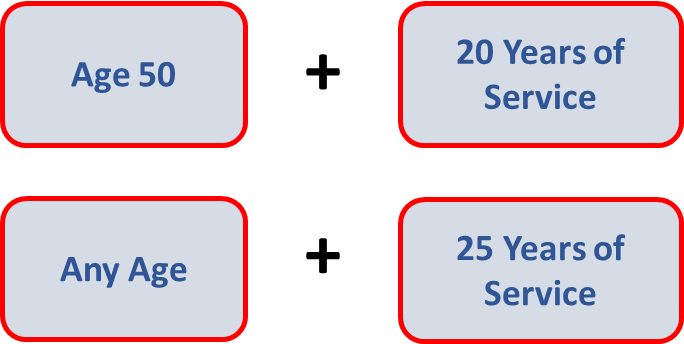

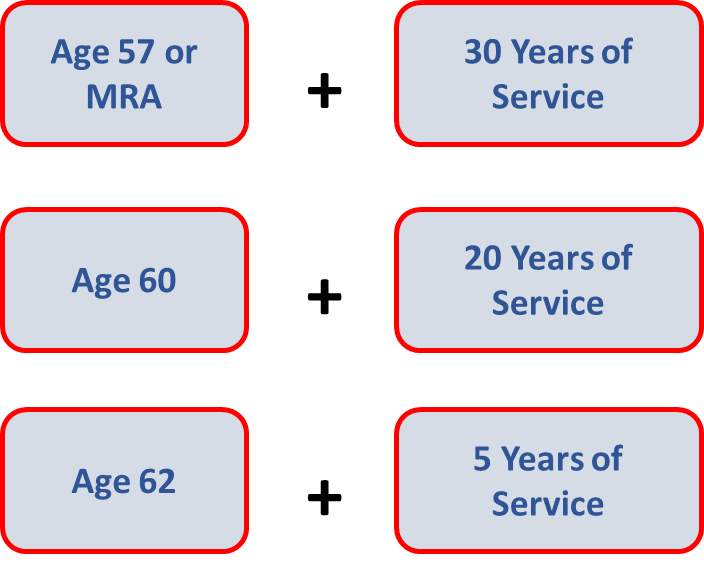

Eligibility to Retire on Immediate Unreduced Pension

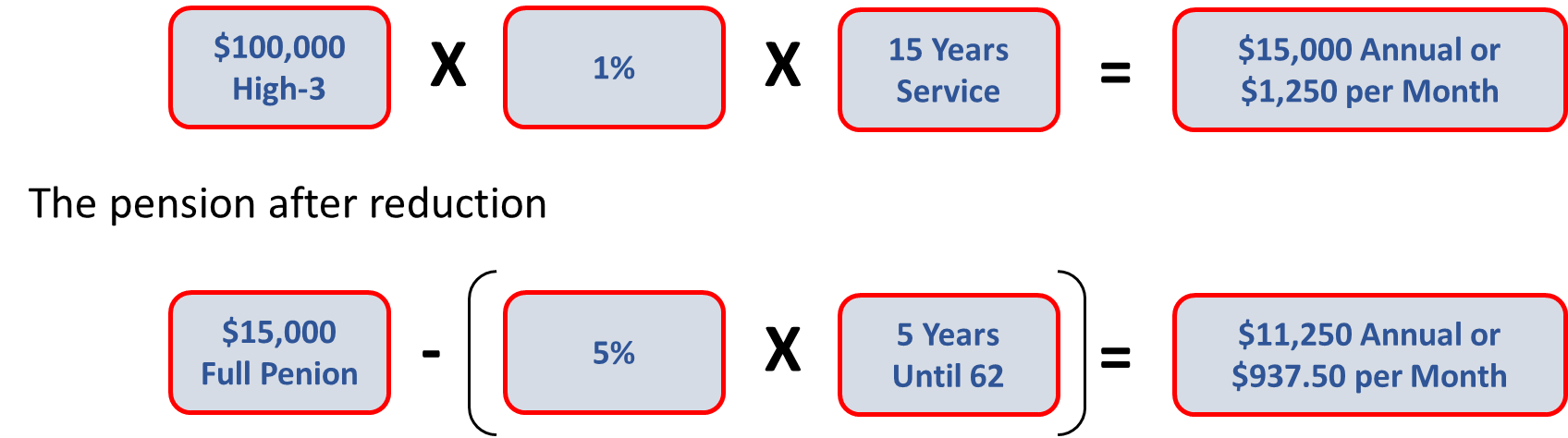

An immediate retirement benefit is one that starts within 30 days from the date you stop working. If you meet one of the following sets of age and service requirements below, you are entitled to an immediate retirement benefit. If you retire at MRA with at least 10 years of service, but less than 30 years of service, your benefit will be reduced by 5% a year for each year you are under 62, unless you have 20 years of service and your benefit starts when you reach age 60 or later.

The early retirement benefit is available in certain involuntary separation cases and in cases of voluntary separations (Voluntary Early Retirement Authority – VERA) during a major reorganization or reduction in force (RIF).

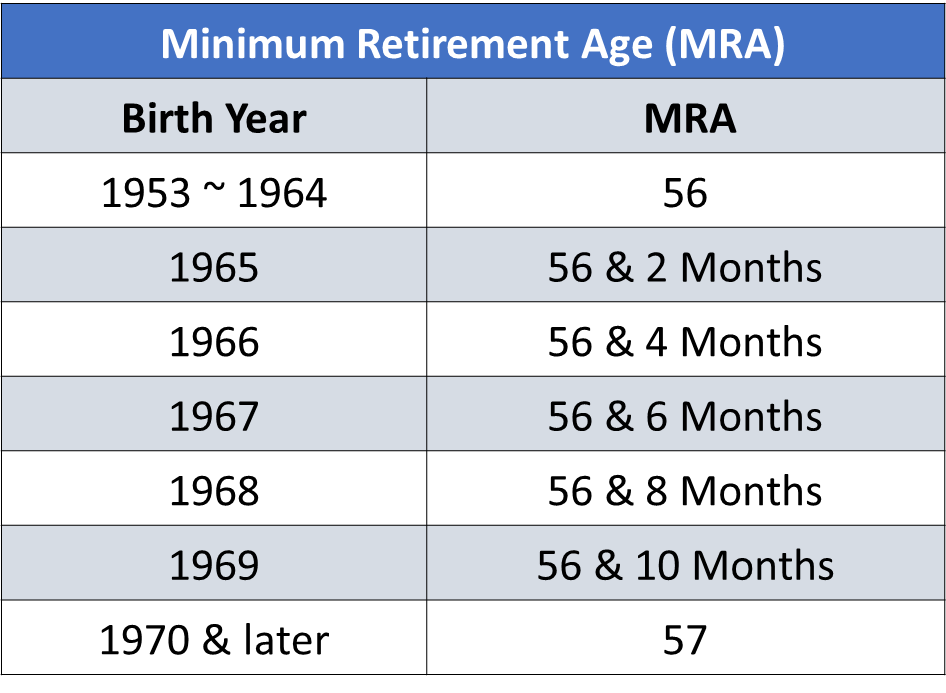

Minimum Retirement Age (MRA) is Dependent on Birth Year

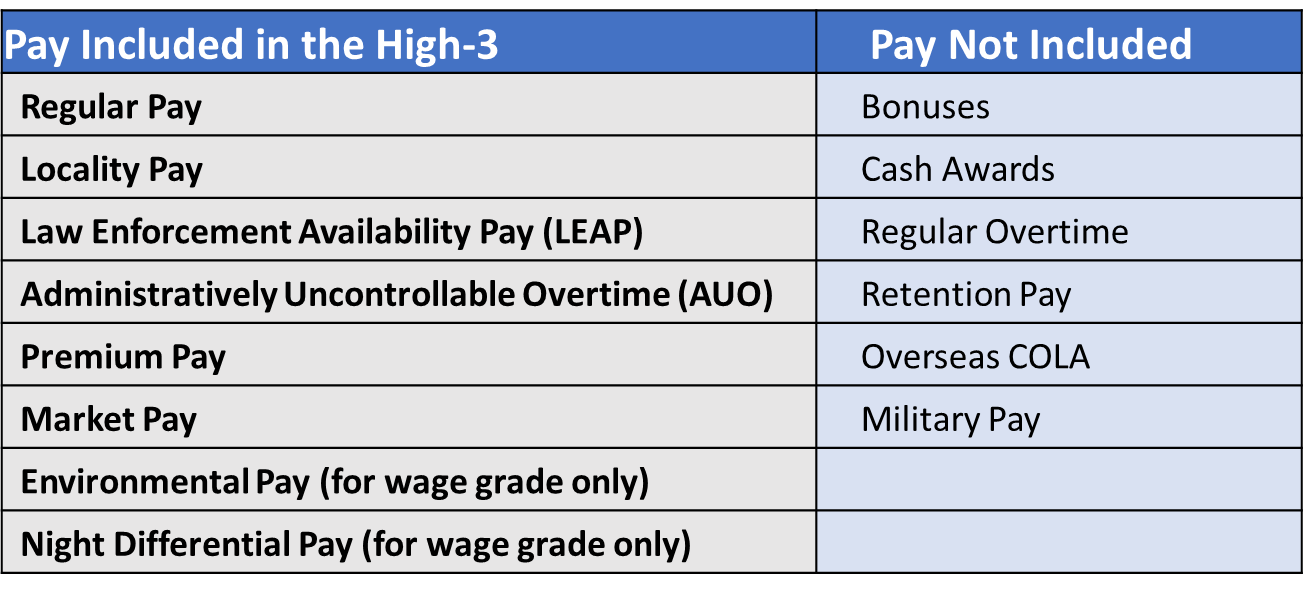

High-3 Calculation

The high-3 salary is the average of the highest 36 months of consecutive income. For most people, the last 36 months are used for calculation purposes, but not always the case. Not all income is included in the high-3. The table below shows what is included and excluded from the high-3 calculation. Learn more about the High-3 calculation here.

Creditable Service Calculation

The calculation includes several components:

- Service time from work

- Unused sick leave

- Military time

- Made deposit to count towards civilian service

- Redeposit service

- Refunded pension contribution when leave

- Non-deductible Service (Temp/Intern)

- Federal service before 1/1/1989 but did not contribute to FERS (must buy back)

If you are buying back your military time, be sure to reference the Military Service Deposit Rules for FERS Service Credit.

Special Note for Active & Reserve Military

Retired military receiving pensions can opt to buy their military time back which will increase the total federal civilian creditable service. Often, it makes sense to do a military buyback if you retired at a low salary (in the military) and have a much higher federal salary. Take the time to run the numbers on buying back military time vs not.

Other special notes:

- Retired reservist can make a military deposit and not lose the military pension

- Combat Time is eligible

- Military Academy is eligible

Do you lose the military pension immediately if you buy-back military time?

A common misconception is that you will lose your military pension immediately. This is NOT true. The military pension will stop once you start receiving an immediate pension from FERS.

Sick Leave Will Increase FERS Pension for Life

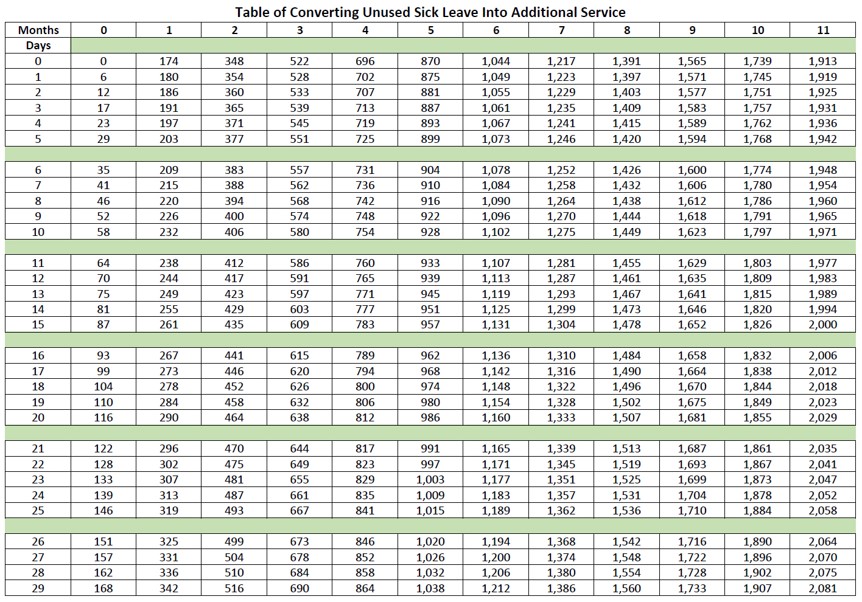

All unused sick leave is converted into months & days of service using the 2087 Chart.

- The converted time is added to your total service time

- Days over 30 will count towards as an additional month of service

- Left over days are discarded

Sick leave only adds to service time and will not count toward eligibility (does not help you retire earlier).

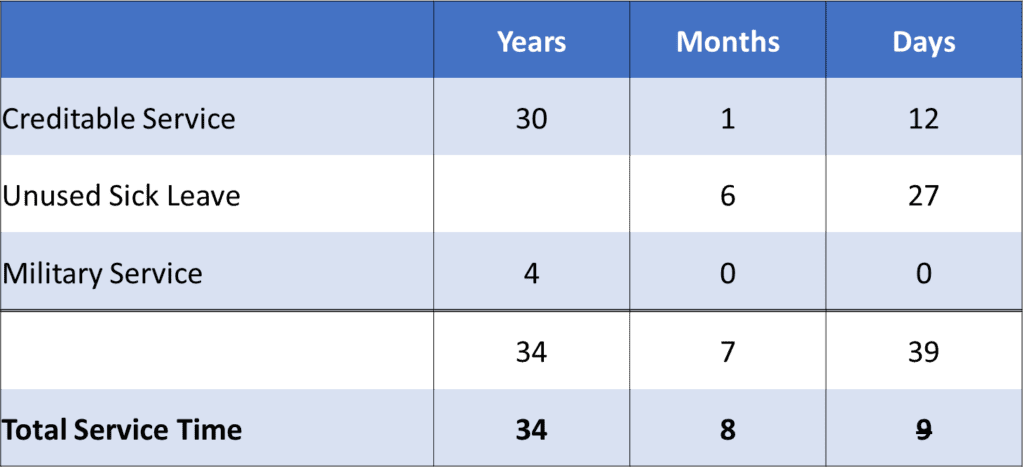

In the example below, there are 6 months and 27 days of unused sick leave. An important note, the sick leave is added to the creditable service time to then round out at 30 days. Any days left over the 30 days is lost. In this example, 9 days of sick leave is forfeited and does not add to the pension. For further details, see our FERS Retirement Sick Leave Calculator.

Calculating creditable service with civilian time, military time, and unused sick leave.

How to Convert Unused Sick Leave

The 2087 chart is used to convert unused sick leave. Determine the total unused sick leave number and locate on the chart rounding down. From there you can find the total months at the column and days by the row.

Calculating Your FERS Pension Amount

Basic Calculation

You will use the basic calculation if you fall under one of the following:

Retiring under age 62 with any number of years of service

OR

Retiring after age 62 with less than 20 years of service

For a simplified overview, see How to Calculate Your FERS Pension – The Short Version.

Bonus Calculation

You will use the basic calculation if:

Age 62 or After With at Least 20 Years of Service

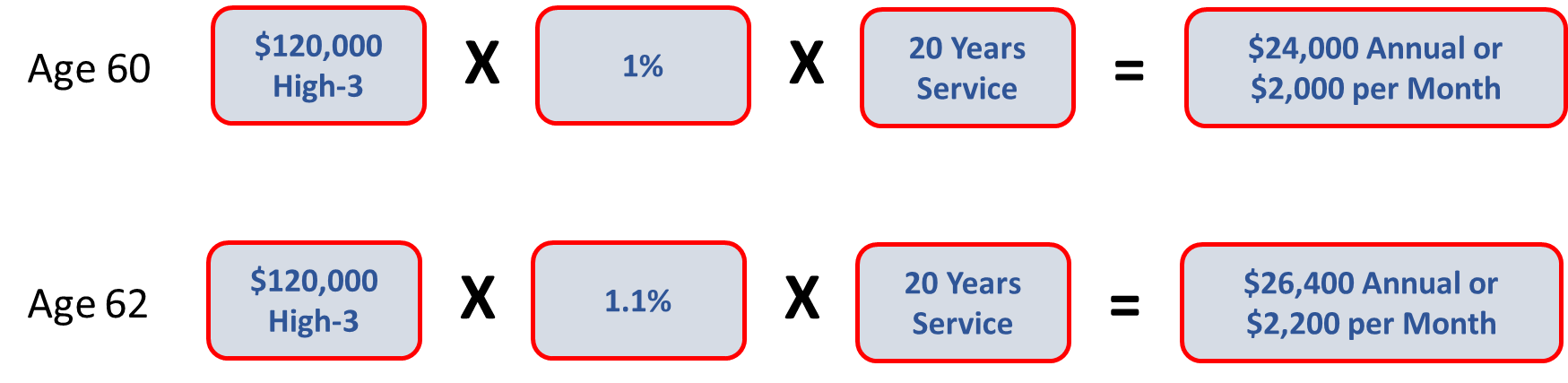

Basic (1%) vs. Bonus Calculation (1.1%) – The 10% Bonus

The decision to retire before age 60 or after 62 can be a game changer for your retirement. In the below example, you can see the increase just by retiring after 62 with the same high-3 and years of service.