FEGLI Basic Life Insurance: Biggest Missed Retirement Benefit for Federal Retirees

Federal Employee Group Life Insurance coverage (FEGLI) is a unique and misunderstood retirement benefit for federal employees. It is unique in the fact that you have the ability to keep it after retirement. Group life insurance policy in the private sector ends when an employee retires. They usually cannot keep their private group life insurance into retirement even if they want to. So why is it that when I meet with federal employees, almost 90% said that they would be dropping or getting rid of FEGLI in retirement? Let’s clarify what the coverages are and what you should consider before making a decision that’s right for you and your family.

FEGLI – The Basic, The Options, and Your Age

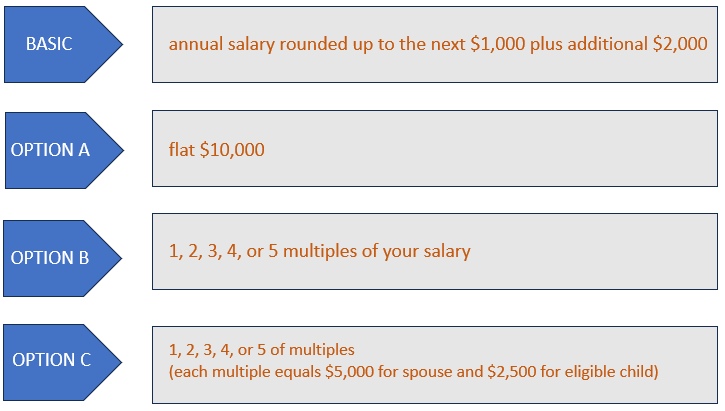

Before we get to retirement, you should understand the kinds of coverage available within FEGLI Options and the amount of basic coverage you have. Here is the breakdown:

- The Basic Coverage is your annual salary (base + locality pay) rounded up to the nearest thousand plus two thousand. So, if your income is $122,343 (GS 12 Step 8, DCB), it will be rounded up to $123,000 + $2,000, so your basic coverage is $125,000.

- Option A is a flat $10,000 of coverage

- Option B is your income rounded up to the nearest thousand multiply the number of multiples you are looking for. So if you have 2 multiples of Option B, using the above pay rate, your Option B coverage would be $123,000 x 2 = $246,000. If you want to see how FEGLI Option B compares to private term coverage, check out Comparing Federal Employee Group Life Insurance (FEGLI Option B) with Term Life Insurance.

- Option C is coverage on your family. If you are married, each multiple is $5,000 for your spouse and $2,500 for each eligible child

The price of the options depends on your age. Even Option C, which covers your family, depends on your age and not theirs. You can read more about the options in our articles below:

Maximizing Federal Employee Group Life Insurance (FEGLI) Benefits

FEGLI ABC – Federal Employee Group Life Insurance Options in Retirement

Transition of FEGLI Basic Coverage into Retirement

Let us focus on basic since it is automatically enrolled when you join federal service and what most employees have at retirement. While you are still working, the cost is reduced, and the government helps pay a portion of the premium. When you retire, you are eligible to continue basic, but the discount and subsidy stop, and you will see a huge jump in premiums. Here is an example.

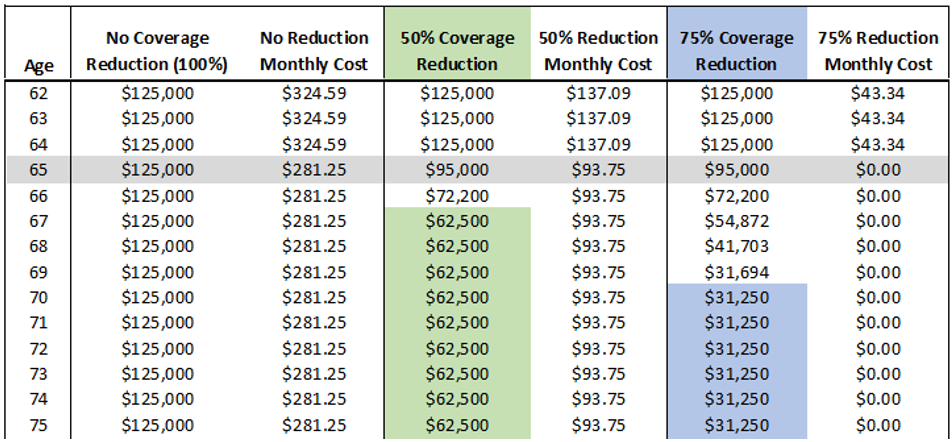

An employee with $125,000 in basic coverage at age 62 would pay $20 per pay period or $43.34 per month. Assuming they retire at age 62, their basic premium would be $324.59 per month.

Most people would see the extra premium for this choice and decide that they will drop basic insurance. When you run retirement estimates from HR, this is also the option that is shown first. This is actually a bit misleading and does highlight the second unique aspect of FEGLI. You have choices on what to keep.

FEGLI Basic Choices in Retirement – No Reduction, 50% Reduction, or 75% Reduction

Not only can federal employees keep FEGLI in retirement, but they can also pick and choose how much coverage they want to keep. The $325.59 monthly premium is only if you keep all of the coverage. If you were to choose a reduction, your cost will decrease significantly. Here are the options and costs

- No Reduction (keeping all coverage) – $324.59 per month

- 50% Reduction (keeping half of the coverage) – $137.09 per month

- 75% Reduction (keeping a quarter of the coverage) – $43.34 per month

The best part is that you only need to pay the premium until you turn 65. After your 65th birthday, all of the premiums will get a $43.34 discount per month. That means, if you picked the last option with 75% reduction, you will pay nothing out of pocket after age 65! It literally becomes free life insurance for the rest of your life.

How Do the Reductions Work?

If you are considering a reduction option for retirement, you are on the right track. Let’s review how the reductions work.

The reduction for FEGLI starts at age 65. So even if you selected a reduction option at 62, you would still keep 100% of FEGLI ($125,000 in our example) regardless of the reduction chosen. After you reach age 65, the coverage will reduce by 2% per month until it reaches your specified reduction coverage amount.

If you are still working, the reduction will start at age 65 or retirement, whichever is later. Here is a chart showing what the coverage and cost would be each year for someone retiring at age 62.

How can federal retirees continue their FEGLI coverage into retirement?

In order to keep FEGLI in retirement, you must have had coverage for 5 years prior to retirement. If you did not have FEGLI or any options for 5 years, you cannot keep it in retirement.

Optimizing Your FEGLI Basic Life Insurance as a Retired Federal Employee

Your decision on coverage should be based on your legacy goals, health, financial situation, and your age. Speaking with a fed-focused advisor or a Chartered Employee Benefits Consultant would make sense before you decide. Even if you decide that you do not need life insurance in retirement, I still suggest you consider the 75 percent reduction option. The reason is simply that it is a great deal. If you retire at age 62, you will pay 3 years of premium. The dollar amount would be $43.34 x 12 months x 3 years = $1,560.24. However, you will receive a $31,250 life insurance policy for free after age 65, not a bad deal.

If you do decide that you do not want any part of FEGLI and are close to retirement, consider keeping it until retirement and select “Full Reduction” instead of dropping it ahead of time. Coverage reduces by 2 percent per month until it is gone so you will have some coverage in your early retirement years.

Reach Out to Us!

If you have additional federal benefit questions, contact our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciaries (AIF®). At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars through our online events. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out, and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting with us now.

About David Fei

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

David has been in the financial services industry for over 20 years, bringing a wide range of experience in personal finance to every client relationship. He specializes in helping federal families tackle life's biggest financial challenges—retirement income planning, educational funding, and investment strategy. David's approach is grounded in education. He believes that when clients truly understand their options, they make better decisions. That's why he takes the time to explain the "why" behind every recommendation.