FEGLI ABC - Federal Employee Group Life Insurance Options in Retirement

If you are a federal employee or annuitant, you may have heard of FEGLI or the Federal Employees’ Group Life Insurance program. FEGLI is a group term life insurance program that provides coverage for federal employees, retirees, and their family members. FEGLI offers four types of coverage: Basic, Option A, Option B, and Option C. Each type of coverage has different features, costs, and choices in retirement. This article will explain how FEGLI options work and how they affect your life insurance coverage and premiums when you retire from federal service.

Enrollment and Life Insurance Coverage for Federal Employees

You may have first signed up for FEGLI life insurance when your federal career started. Like in the private sector, everyone can sign up for group life insurance without proof of insurance. However, after that, you cannot sign up for additional coverage during open season. If you want to sign up or add coverage, you must take a physical exam and go through medical underwriting. See SF 2822 for additional information.

The second opportunity to add coverage is when you have a qualifying life event. These situations are changes in your personal/family where you should review the amount of life insurance you carry.

Qualifying Life Events for FEGLI are:

- Marriage

- Divorce

- Spouse’s death

- Birth or adoption of a child

You have 60 days to submit a completed SF 2817 form to your human resources office to increase your coverage. You can only submit the form after the event has occurred. You cannot submit it prior to the event.

The third opportunity is with FEGLI open season. However, this is very rare, and the last FEGLI open season was in 2016 and 2004

Lastly, you can decrease coverage at any time. You would use the same SF 2817 form and submit it to HR.

Eligibility to maintain FEGLI in retirement

The fact that you can keep group life insurance coverage into retirement is unique. Private section group life doesn’t offer this at all. However, there is a 5-year coverage requirement. It means that you have to continue coverage for 5 years prior to retirement to keep that coverage. If you added options before retirement, it must be kept for 5 years before it is eligible.

FEGLI Coverage into Retirement

Now that we have reviewed eligibility requirements, let’s look into each section of The Federal Group Life Insurance benefit and how it will be carried into retirement. To assist with the concept, we should use an example employee.

Employee (Bob) is married and has 2 children (age 23 and 20. He is a Grade 12 Step 10 employee, base+localy pay is $122,459. He has the maximum coverage of Basic, Option A, Option B x 5, and Option C x 5. He plans to retire at age 62.

FEGLI Basic Insurance Coverage – the Biggest Missed Benefit for FERS Retirees

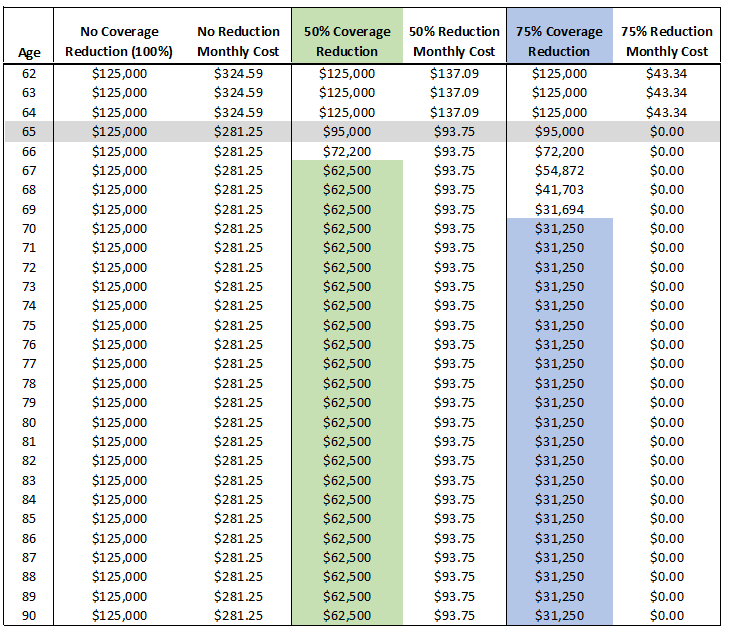

Basic life insurance is the biggest missed benefit for FERS retirees. Let’s start with understanding this coverage. Basic is your current income (base+locality), rounded up to the nearest thousand + $2,000. So in Bob’s case, his basic coverage is $125,000 ($122,459 rounded up, which is $123,000 + $2,000 = $125,000). When Bob is still working, the monthly cost is $43.34 ($20 per pay period). However, after he retires, the monthly cost will jump to $324.59. Most people will look at the price jump and immediately drop this optional insurance. This is a huge mistake.

You have options! The cost is only that high if you keep the entire $125,000 coverage. If you choose to elect a reduction in coverage. The costs are reduced significantly. This chart will highlight the cost reduction with each reduction option.

Additional Options

Since Bob has the maximum amount of coverage, the goal is to review what each option means and look at how the cost changes in retirement.

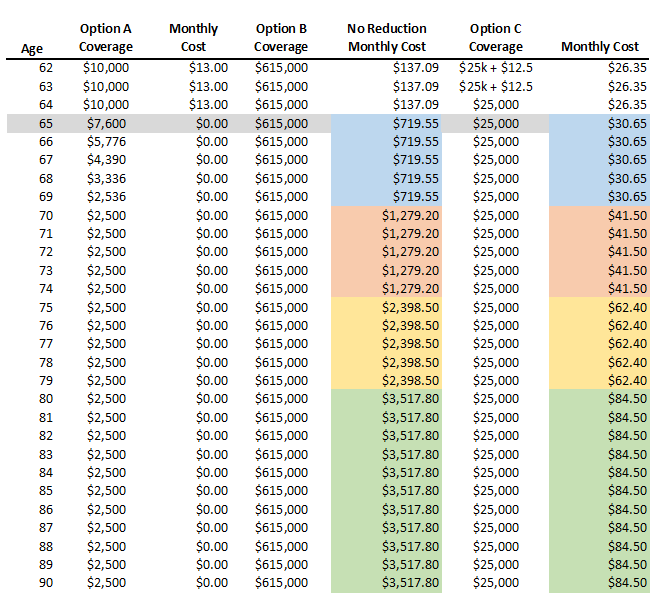

– Option A: Flat $10,000

The amount of insurance is set and cannot be changed by the employee. The cost of Option A changes every 5 years. At retirement or age 65 (whichever is later), this coverage will automatically reduce by 2% per month until there’s $2,500 left. Moreover, as long as you keep the FEGLI basic coverage, this insurance is free after retirement.

– Option B: Income Multiples

This is the additional times of basic income you can elect. Bob’s five multiples of Option B so the amount is his annual income (basic + locality) rounded up to the nearest thousand x multiple elected ($122,459 rounded up to $123,000 x 5 = $615,000). The caution is that the cost of Option B jumps every five years. In retirement, you can avoid this cost by electing full reduction. The amount of insurance will be reduced by 2% per month until it is depleted. The cost increase eventually stops at age 80. As you can see in the chart below, the costs are extremely high. For more considerations on this topic, you might review comparing FEGLI Option B with private term life insurance.

– Option C: Coverage for Spouse and Children

Bob also has five multiples of Option C, which provides coverage for his spouse and children under age 22. Although it covers multiple people, there is no additional cost. It also means no cost reduction when children become ineligible for coverage.

In this case, his spouse and his youngest child have five multiples of coverage. His older child is no longer eligible since he is over the age limit. Also, the amount for spouse and children are different. For spouse, each multiple is $5,000. For eligible children, it is $2,500 per multiple.

Detailed Chart

To illustrate the different coverage and ongoing costs, see the chart below:

Knowledge is Confidence!

What Should You Do?

For most, FEGLI may be something you have paid for your entire career. Doesn’t it make sense to keep a portion of it for free for the rest of your life? I would say that everyone should elect the 75% reduction option. That’s a no-brainer. However, depending on your health, family’s life expectancy, and financial situation, keeping other life coverage in may be beneficial. The costs seen in this article are high, but that assumes you keep all of the coverage. You can drop a few multiple before retirement and manage the expense. Do not let this unique employee benefit go without some careful consideration. Reach out to us for a personalized retirement benefits report.

Personalized Retirement Benefits Report

If you have additional federal benefits questions, work with financial advisors for federal government employees. Our team of CERTIFIED FINANCIAL PLANNER™ (CFP®) and Charter Federal Employee Benefits Consultant (ChFEBC℠). Retirement planning workshops for federal employees are coming soon so keep a look out!

Reach Out to Us!

If you have additional federal benefit questions, reach out to our team of CERTIFIED FINANCIAL PLANNER™ (CFP®) and Chartered Federal Employee Benefits Consultants (ChFEBC℠). At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars through this link. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Interested in having PlanWell host a federal retirement seminar for your agency? Reach out, and we can collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting.

About David Fei

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

David has been in the financial services industry for over 20 years, bringing a wide range of experience in personal finance to every client relationship. He specializes in helping federal families tackle life's biggest financial challenges—retirement income planning, educational funding, and investment strategy. David's approach is grounded in education. He believes that when clients truly understand their options, they make better decisions. That's why he takes the time to explain the "why" behind every recommendation.