Federal Retirement MRA

What is the Minimum Retirement Age (MRA) for Federal Employees?

Understanding Minimum Retirement Age (MRA)

The Minimum Retirement Age (MRA) is the earliest age at which a federal employee can retire with an immediate retirement benefit under FERS. The MRA varies based on an employee’s birth year but generally falls between 56 and 57 years. Reaching your MRA opens up various retirement options and forms the cornerstone of retirement planning for federal employees. The concept of MRA is vital in determining when one can begin to draw retirement benefits without penalty, though other conditions related to years of service must also be satisfied.

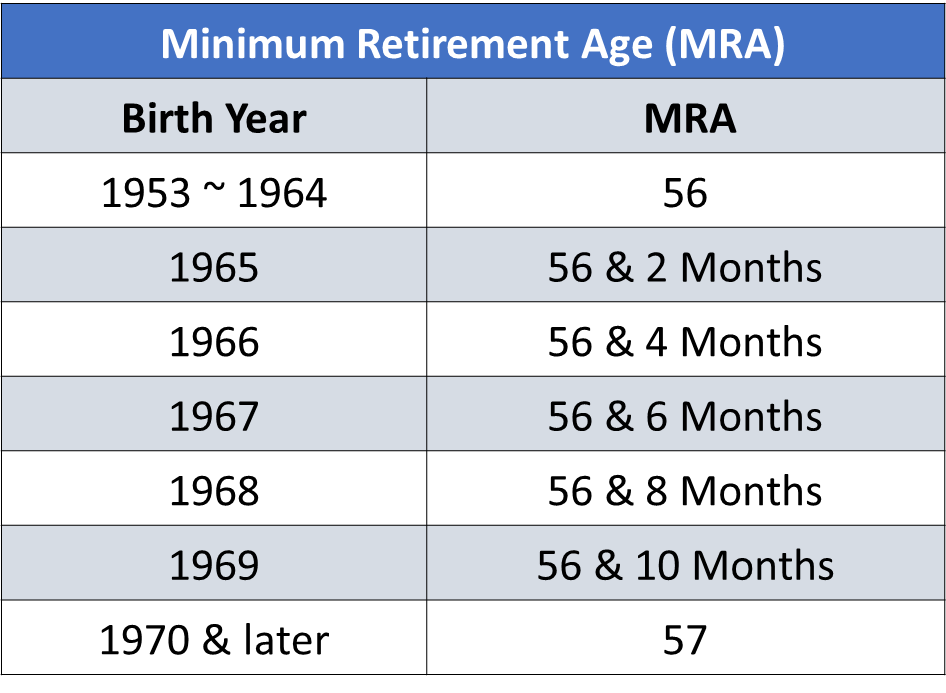

How to Calculate Your MRA

To calculate the MRA, federal employees need to consider their birth year:

Impact of MRA on Retirement Planning

The MRA significantly impacts retirement planning for federal employees. Retiring at or after reaching your MRA usually avoids reductions in annuity benefits, provided other service requirements are met. If opting for the MRA+10 retirement, employees can retire as early as their MRA with at least 10 years of service but will face either annuity reductions or a postponed retirement. Thus, MRA serves as a pivotal milestone in plotting out retirement dates, understanding annuity calculations, and ensuring maximum retirement benefits. Planning accordingly around one’s MRA ensures a smoother transition to retirement.

For more information on the difference between a deferred and postponed article check out: Deferred vs Postponed Retirement – Avoid Common Mistakes!

Below we will go into more detail about the FERS MRA. If you are interested in learning more about the Federal Employee Retirement System (FERS), check out the Complete Guide to FERS – Federal Employee Retirement System.

Federal Employees Retirement System (FERS) Eligibility and Minimum Retirement Age (MRA) Considerations

The Federal Employees Retirement System (FERS) is an essential program that provides retirement benefits to federal employees. Understanding the nuances of FERS eligibility and the Minimum Retirement Age (MRA) is crucial for federal employees planning their retirement. This article delves into the intricacies of FERS, how it compares to other plans, the determination of MRA, and the various types of retirements and their benefits.

What is the Federal Employee Retirement System (FERS)?

Overview of FERS

FERS, or the Federal Employee Retirement System, is a retirement plan for federal employees in the United States. Designed to provide comprehensive retirement benefits, FERS includes three key components: the Basic Benefit Plan, Social Security, and the Thrift Savings Plan (TSP). Established in 1987, FERS was developed to succeed the Civil Service Retirement System (CSRS) and offers a more modern approach to retirement compared to its predecessor.

Components of FERS Retirement

The components of FERS retirement are pivotal to understanding the system’s functionality. The Basic Benefit Plan requires contributions from both the employee and the federal government, yielding a monthly annuity upon retirement. Social Security, contributed to throughout one’s career, is the second component and provides a base level of retirement income. The Thrift Savings Plan (TSP), akin to a 401(k), allows employees to make additional retirement contributions, with agency matching up to certain limits, resulting in a more tailored retirement savings plan.

FERS vs. Other Retirement Plans

When compared to other retirement plans, FERS offers unique advantages and challenges. Unlike private sector 401(k) plans, FERS provides a guaranteed annuity alongside Social Security benefits. Additionally, the TSP offers the benefit of federal matching contributions. Contrasting with the older Civil Service Retirement System (CSRS), FERS generally requires lower employee contributions and includes Social Security integration, making it more comprehensive albeit slightly less generous in terms of pure pension.

What is the Federal Retirement MRA for Federal Employees?

Definition of Federal Retirement MRA

The Minimum Retirement Age (MRA) is a critical element in determining when a federal employee can retire under FERS. Defined by the Office of Personnel Management (OPM), MRA varies based on the employee’s year of birth, ranging from age 56 to age 57. The MRA signifies the earliest age at which an employee can elect to retire with immediate retirement benefits, provided they meet other service requirements.

MRA+10 Retirement Option

One of the flexible options under FERS is the MRA+10 retirement. This provision allows employees who have reached their MRA and have at least 10 years of service to retire. However, the annuity payments are typically reduced by five percent for each year the employee is under age 62. This option serves those who wish to retire early but must be weighed against the potential reduction in long-term benefits.

Who is eligible for FERS Retirement?

Eligibility Criteria for Immediate Retirement

Immediate retirement under FERS requires federal employees to meet specific age and service requirements. Generally, employees must satisfy one of the following: an MRA federal retirement with 30 years of service, age 60 with 20 years of service, or age 62 with five years of federal service. Meeting these criteria allows employees to retire with full benefits and avoid early retirement reductions.

Requirements for Early Retirement

Early retirement options are available under FERS for employees who leave federal service before meeting standard criteria. This is often seen in cases of voluntary early retirement for those with at least 25 years of service or if they reach age 50 with 20 years of service during periods of workforce restructuring or downsizing. Early retirement offers reduced benefits but can be an essential option for those seeking flexibility or facing mandatory agency reductions.

Deferred Retirement Eligibility

Deferred retirement is a critical component for those who leave federal service before meeting immediate retirement age and service requirements. Employees who complete at least five years of service can defer their retirement benefits until they reach age 62. Alternatively, with at least 10 years of service and upon reaching MRA federal retirement, employees can elect for MRA+10 federal retirement, albeit with reduced benefits. Deferred retirement ensures that service years still count toward future benefits.

What are the different types of FERS Retirement?

Immediate Retirement Options

Immediate retirement is often the most straightforward for those who meet age and service requirements. Under FERS, employees can retire with full benefits once they reach their MRA federal retirement and have the requisite 30 years of service, or they can retire at age 60 with 20 years, or age 62 with as little as five years of service. Immediate retirement provides a steady annuity reflecting years of creditable service and average salary.

Understanding Deferred Retirement

Deferred retirement under FERS serves those who leave federal employment before they qualify for immediate retirement. An employee with at least five years of creditable service can defer retirement benefits until age 62. This means they will not receive retirement benefits immediately upon leaving federal service but are still eligible for an annuity, which ensures financial benefits later in life.

Disability Retirement Benefits

FERS also provides disability retirement benefits to federal employees who are unable to continue working due to disability. To qualify, an employee must have at least 18 months of federal service and demonstrate the inability to perform their job due to a medical condition. The Office of Personnel Management (OPM) must approve the application, and benefits include continued annuity payments calculated to partially replace lost income, assisting those who can no longer work.

How are retirement benefits calculated for FERS?

Basic Calculation Formula

The calculation of FERS retirement benefits involves several factors. The basic formula considers an average of the highest three consecutive years of salary, known as the “high-3” average salary. This figure, multiplied by a percentage factor which is based on years of creditable service and age at retirement, establishes the annual annuity. For example, the percentage factor is typically 1% of the “high-3” per year of service, or 1.1% for those retiring at age 62 or later with at least 20 years of service.

Impact of Years of Service

The number of years of creditable service significantly impacts retirement benefits under FERS. Employees with 30 years of service are entitled to higher benefits compared to those with shorter service periods. Each year of additional service not only increases the annuity calculation percentage but also ensures a higher final retirement payout, providing greater financial stability.

Effect of Age on Annuity Payments

Age plays a critical role in determining FERS annuity payments. Retiring at the standard age thresholds (MRA, 60, or 62) ensures maximum benefits, while early retirement options like MRA+10 federal retirement result in reduced annuity payments due to penalties. Those who can defer collecting benefits until age 62 with substantial years of service benefit from a higher percentage multiplier, increasing their overall retirement annuity.

Understanding Retirement Eligibility under the Federal Employees Retirement System (FERS): Minimum Retirement Age (MRA) and More

The Federal Employees Retirement System (FERS) is a retirement plan that covers employees of the United States federal government. Introduced in 1987, FERS replaced the older Civil Service Retirement System (CSRS) and includes a combination of Social Security benefits, a Basic Benefit Plan, and the Thrift Savings Plan (TSP). Understanding the nuances of FERS, particularly the MRA federal retirement and related retirement provisions, is crucial for any federal employee planning their retirement. This article delves into the FERS structure, eligibility criteria, and various retirement options to help federal employees navigate their path to a secure retirement.

What is the Federal Employees Retirement System (FERS) and How Does It Work?

Overview of FERS

The Federal Employees Retirement System (FERS) is a comprehensive retirement system created to ensure that federal employees can retire with financial stability. FERS includes three key components: Social Security benefits, the Basic Benefit Plan, and the Thrift Savings Plan (TSP). Each of these components works together to provide a robust retirement benefit package. FERS covers most employees who joined the federal workforce after 1983, replacing the older Civil Service Retirement System (CSRS).

Components of the FERS Benefits

FERS benefits are comprised of three main parts: – The Basic Benefit Plan: This is a defined benefit plan where both the employee and the federal government make contributions. Upon retirement, employees receive an annuity based on their years of service and the average of their highest-earning three consecutive years. – Social Security: Federal employees under FERS are covered by Social Security, contributing a portion of their salary throughout their federal employment. Upon reaching eligibility, they receive Social Security benefits. – Thrift Savings Plan (TSP): The TSP is a defined contribution plan similar to a private sector 401(k). Federal employees contribute to this plan and can receive matching contributions from the government. The TSP account grows tax-deferred until withdrawal during retirement.

Eligibility Criteria for FERS

Eligibility for FERS retirement benefits hinges on a combination of years of service and age. To retire under FERS with an immediate annuity, federal employees must meet minimum age and service requirements. Typically, eligibility is achieved through:

- Age 62 with 5 years of service

- Age 60 with 20 years of service

- Minimum Retirement Age (MRA) with 30 years of service

- MRA with 10 years of service, although this option comes with a permanent reduction to the annuity.

How Does the MRA+10 Retirement Option Work?

Eligibility for MRA+10 Retirement

The MRA+10 retirement option allows federal employees to retire upon reaching their Minimum Retirement Age with as little as 10 years of creditable service. This option benefits those who wish to leave federal service earlier than the standard service retirement scenarios. However, choosing this path comes with significant considerations. Specifically, an employee’s annuity will be permanently reduced by 5% for each year under age 62, which can considerably impact the overall retirement benefit.

Advantages and Disadvantages of MRA+10

One of the primary advantages of the MRA+10 retirement option is the flexibility it offers to those who have accumulated sufficient years of creditable service but have not reached the typical age or service thresholds for a full retirement benefit. This flexibility can be advantageous for those looking to switch careers or who need to retire early for personal reasons. On the downside, the major disadvantage is the reduction in annuity, which could significantly lower the financial stability of one’s retirement unless additional savings or income sources are planned.

How to Apply for MRA+10

Applying for MRA+10 retirement involves several steps. Initially, employees should ensure they meet the MRA and years of service requirements. Next, they need to fill out the appropriate FERS retirement application forms provided by the Office of Personnel Management (OPM). Documentation proving eligibility, such as records of federal employment and service credits, should accompany the application. Finally, upon submission, the OPM processes the application and calculates the annuity considering the reduction factors for retirement before age 62. Thorough planning and careful consideration of the financial impact are essential before opting for MRA+10.

What Are the Requirements for Early Retirement under FERS?

Eligibility for Early Retirement

Early retirement under FERS is available under specific circumstances, often tied to downsizing or restructuring within federal agencies. Eligibility for early retirement typically requires:

- Age 50 with 20 years of service

- Any age with 25 years of service. This type of retirement is generally offered during periods of significant workforce reduction and provides certain incentives for employees to retire earlier than typical eligibility would allow.

Reduction in Annuity for Early Retirement

Choosing early retirement usually results in a reduced annuity. Employees under age 62 who retire early will see a reduction in their annuity similar to the MRA+10 scenario. The reduction is typically 5% for each year under age 62, which can notably lessen the retirement income unless balanced by other retirement savings or benefits. Those considering early retirement must weigh this potential reduction against their immediate retirement needs and future financial security.

Service Credit and Years of Service Considerations

Both service credit and years of service play crucial roles in determining FERS eligibility and the computations of retirement benefits. Service credit encompasses periods of federal employment that count towards retirement eligibility and annuity calculations. Additional service credits can be obtained through unused sick leave or repurchasing prior federal service. Proper documentation and verification of years of service by the OPM are essential steps in ensuring accurate annuity calculations and eligibility for various retirement types under FERS.

What is the Role of Years of Service and Age in Determining FERS Retirement Eligibility?

Service Retirement and Immediate Retirement Eligibility

Service retirement under FERS requires meeting specific combinations of age and years of service:

- Age 62 with 5 years of service

- Age 60 with 20 years of service

- MRA with 30 years of service. Immediacy in retirement benefits depends on these thresholds, ensuring no delay in receiving annuity payments post-retirement. Understanding these combinations helps federal employees plan their careers and retirement timelines more effectively.

Understanding Annuity Calculations

Annuity calculations under FERS are determined based on the highest three years of earnings (the High-3 average) and years of creditable service. The basic FERS annuity formula is: – 1% of your High-3 average salary multiplied by years of service (or 1.1% if retiring at age 62 or later with at least 20 years of service). Additional adjustments may apply based on factors such as the type of retirement chosen and whether contributions to the retirement fund have been forfeited or refunded in the past. Accurate annuity calculations ensure a stable and predictable retirement income stream.

Considerations for Deferred and Disability Retirement

Deferred retirement is for federal employees who leave service before reaching retirement age but have at least five years of creditable service. They can apply for benefits once they reach retirement age. Disability retirement is available to employees with at least 18 months of service, declared unable to perform their duties due to a medical condition. Both options provide alternative pathways for those unable to meet the standard retirement age and service requirements, ensuring they still receive benefits under specific conditions and within defined timelines.

How to Apply and Plan for Retirement under FERS?

Steps to Apply for FERS Retirement

Applying for FERS retirement involves multiple steps:

- Confirm eligibility by calculating age, service credit, and MRA.

- Complete the retirement application forms, including the appropriate FERS forms and possibly forms for Social Security and the Thrift Savings Plan.

- Gather required documentation, including employment history, service credit records, and proof of eligibility.

- Submit the application to the Office of Personnel Management (OPM). Employees should start this process well ahead of their planned retirement date to account for processing time and ensure a smooth transition.

Documents Needed for Application

Documents required for a FERS retirement application include:

- Completed retirement application forms,

- Proof of federal employment and service credits,

- Birth certificates or proof of age,

- Marriage certificates (if applying for survivor benefits), and

- Financial records for calculating annuities.

Thorough and accurate documentation helps prevent delays in processing and ensures the correct calculation of retirement benefits.

Role of OPM in Processing Retirement Applications

The Office of Personnel Management (OPM) is responsible for processing all federal retirement applications. They verify the information provided, validate years of service, calculate annuities, and manage the disbursement of retirement benefits. The OPM serves as the central authority ensuring all provided data is accurate and compliant with federal retirement regulations. Understanding their role helps federal employees navigate the retirement process confidently and efficiently.

At PlanWell, our specialized team of Chartered Federal Employee Benefits Consultant® (ChFEBC®), CERTIFIED FINANCIAL PLANNER™ (CFP®), and AIF® professionals is dedicated to guiding you through every step of your FERS retirement journey. If you need a financial advisor for federal employees to ensure you’re making the best decisions about your TSP, MRA, or FERS benefits, we can help you retire with confidence.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.