Understanding the Differences Between FERS Deferred and Postponed Retirement Options

Retirement planning for federal employees involves a complex array of choices and implications, especially when navigating through the Federal Employees Retirement System (FERS). Understanding these options, specifically the nuances between FERS Deferred Retirement and FERS Postponed Retirement, is crucial for any federal employee planning their exit from federal service. This article aims to outline the eligibility requirements, discuss the benefits and limitations, and explore the impacts on other federal benefits. For a more detailed discussion, feel free to check out our comprehensive guide on Deferred vs Postponed Retirement.

Deferred & Postponed Retirement

If you leave federal service before you meet the age and service requirements for an immediate retirement benefit, you may be eligible for deferred federal retirement benefits. To be eligible, you must have completed at least 5 years of creditable civilian service. You may receive benefits when you reach one of the following ages:

- 62 and 5 years

- 60 and 20 years

- MRA and 30 years

A deferred and postponed retirement will avoid the 5% penalty reduction to your annual pension. Essentially, you would be delaying your pension to a later date in lieu of an immediate pension. Be careful! Deferred vs. postponed are very different in the benefits you get to retain into retirement.

To simplify the difference, a deferred federal retirement is if you leave service BEFORE MRA and a postponed retirement is if you leave AFTER MRA.

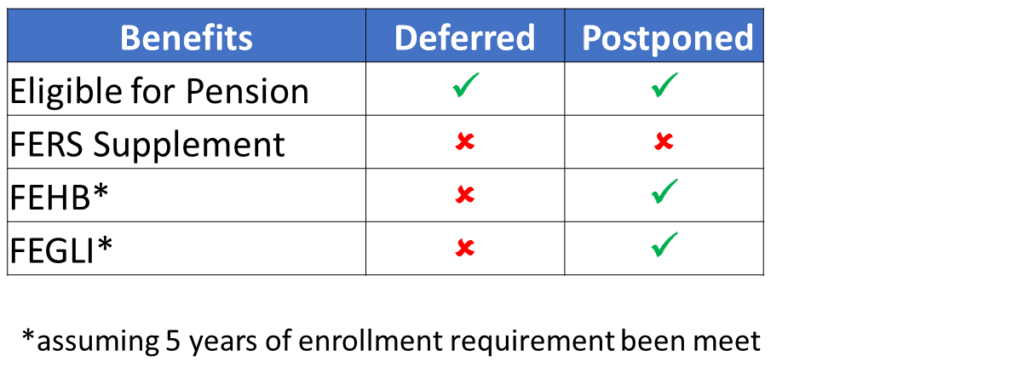

Losing Certain Benefits in Retirement

A deferred federal retirement is not eligible for a Special Retirement Supplement (SRS), FEHB, and FEGLI. Losing FEHB in retirement is a huge loss. The Federal Government continues to pay ~72 – 75% of the FEHB premium even in retirement.

A postponed retirement allows you to keep FEHB & FEGLI once your pension begins. In the interim, there will be no FEHB or FEGLI coverage. In addition, there is no SRS.

What Is the Difference Between FERS Deferred and Postponed Retirement?

Defining FERS Deferred Retirement

FERS Deferred Retirement is an option available to federal employees who leave federal service before becoming eligible for immediate retirement. To qualify, one must have a minimum of 5 years of federal service. Opting for deferred federal retirement means an employee can receive a retirement benefit at a later date, specifically after reaching age 62, or at the minimum retirement age (MRA) with at least 30 years of service. However, it’s crucial to understand that taking this route means forfeiting the right to reenroll in the Federal Employees Health Benefits (FEHB) program upon retirement.

Breaking Down FERS Postponed Retirement

FERS Postponed Retirement is akin to deferred retirement but with key distinctions that benefit those eligible. This type of retirement allows a federal employee to delay the start of their benefits without the loss of benefits that come with deferred retirement. Federal employees opting for this must meet specific criteria, including reaching their MRA and having between 10 and 30 years of service. This option is most beneficial for those looking to avoid the age reduction in their retirement benefits.

Key Distinctions Between Deferred and Postponed Retirement

The primary difference lies in the eligibility for reenrollment in health and life insurance benefits. Postponed retirement offers the chance to reenroll in the FEHB and Federal Employees’ Group Life Insurance (FEGLI), whereas deferred does not. Additionally, the age and years of service required to avoid penalties differ significantly. Choosing between deferred and postponed retirement options requires a comprehensive understanding of these nuances to make an informed decision that best suits one’s financial and health benefit needs.

How Do I Qualify for FERS Deferred or Postponed Retirement?

Eligibility Criteria for FERS Deferred Retirement

Qualifying for FERS Deferred Retirement demands that an employee have at least 5 years of creditable federal service and that they leave their federal position before reaching eligibility for immediate retirement. It’s an option that exists regardless of age, but drawing benefits can only begin after reaching age 62, or earlier if they have more than 30 years of service but must wait until the MRA. Such clear-cut criteria ensure that even those who separate from federal service early have a retirement benefit to look forward to, albeit with specific limitations.

Qualifying for FERS Postponed Retirement

For FERS Postponed Retirement, the requirements are slightly more nuanced. Firstly, an employee must reach their MRA and have at least 10 years of service, but less than 30, to postpone their retirement benefit without incurring the age reduction penalty. Those with 30 years of service can retire at their MRA, and choosing postponement can further enhance their retirement income by eliminating the age penalty. This option is pivotal for employees aiming to maximize their retirement benefits while maintaining eligibility for federal health and life insurance benefits upon retirement.

Understanding Minimum Retirement Age (MRA) for Both Retirement Types

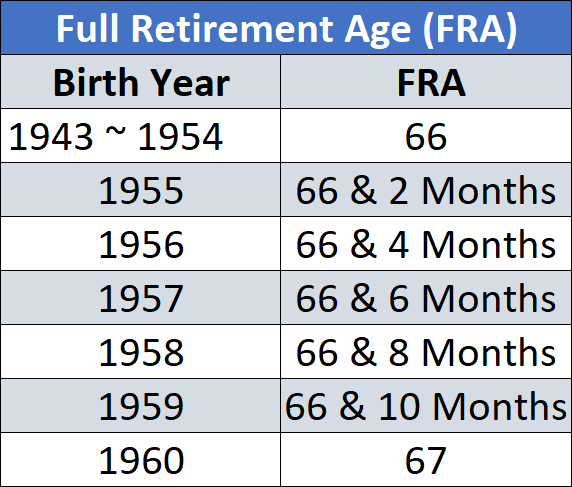

The Minimum Retirement Age is a critical factor in both deferred and postponed retirement. The MRA varies depending on the birth year of the employee, ranging from age 55 to 57. Achieving this age is a prerequisite for postponed retirement and a determining factor for when one can begin receiving deferred retirement benefits without penalties, provided they have the requisite 30 years of service. This underscores the importance of the MRA in planning one’s retirement strategy within the federal system.

What Are the Benefits of Choosing Deferred or Postoned Retirement?

Advantages of FERS Deferred Federal Retirement

Choosing FERS Deferred Retirement can be advantageous for former federal employees who left federal service early and do not need immediate access to their retirement benefits. It provides a safety net, ensuring that years of service contribute towards a future retirement benefit. Although it lacks immediate health benefits, it’s a viable option for those with alternative health coverage and primarily focused on securing a deferred annuity.

Benefits of Opting for FERS Postponed Retirement

FERS Postponed Retirement, on the other hand, greatly benefits individuals by allowing them to delay receiving benefits to avoid early age reduction penalties while retaining the eligibility to reenroll in FEHB and FEGLI programs upon commencing their annuity. This strategic postponement not only enhances the retirement benefit but also safeguards access to essential federal health benefits, making it an attractive option for those eligible.

How to Avoid the Age Reduction in Benefits

Avoiding the age reduction in benefits is a significant concern for many considering deferred or postponed retirement. For deferred federal retirement, receiving benefits without an age penalty requires waiting until age 62, 60 or the MRA with 30 years of service. Postponed retirement allows for the avoidance of such penalties by delaying benefit commencement until meeting the necessary criteria, such as reaching the MRA with at least 10 years of service. This maneuver is essential for maximizing retirement income while minimizing financial drawbacks.

Can I Apply for FERS Disability Retirement if I Choose Deferred Federal Retirement or Postponed Retirement?

Differences Between Disability, Deferred, and Postponed Retirement

The FERS retirement system provides different pathways for employees under varying circumstances. Disability retirement is intended for those unable to perform their duties due to a medical condition, a significantly different criterion when compared to deferred or postponed retirement. Notably, disability retirement can provide immediate benefits under certain conditions, a stark contrast to the deferred options which are predicated on age and years of service.

Eligibility for FERS Disability Retirement

Eligibility for FERS Disability Retirement requires that an employee has at least 18 months of federal civilian service and provides medical documentation of a disability that precludes performance of their current duties. This option is available regardless of age, making it accessible for those who encounter unforeseen health issues. It’s crucial for employees considering this route to understand that opting for disability retirement might affect their eligibility for deferred or postponed retirement options.

Impact of FERS Disability Retirement on Deferred or Postponed Options

Choosing FERS Disability Retirement has implications for deferred or postponed retirement options. Specifically, once an employee opts for disability retirement, they generally cannot switch to deferred or postponed retirement later. This is because each type of retirement serves different needs and eligibility requirements. Therefore, a clear understanding of one’s long-term objectives and health status is essential before making a decision.

What Happens to My Federal Benefits if I Leave Federal Service Early?

Effect on the Federal Employees Health Benefits (FEHB) Program

Leaving federal service early has significant implications for eligibility for the FEHB program. Employees choosing deferred federal retirement forfeit the possibility to reenroll in FEHB when they begin receiving retirement benefits. Conversely, those opting for postponed retirement maintain their eligibility, making it a crucial consideration for anyone dependent on federal health benefits.

Retirement Benefits Considerations for Early Leavers

For those leaving federal service before reaching eligibility for immediate retirement, the choice between deferred and postponed retirement has notable implications for their future benefits. Deferred federal retirement allows for a future annuity but without immediate health benefits, whereas postponed retirement can offer enhanced benefits and health coverage upon meeting specific conditions. The right choice varies based on individual health coverage needs and financial planning strategies.

Strategies to Maximize Retirement Benefits After Leaving Federal Service

To maximize retirement benefits after leaving federal service early, carefully consider the specific requirements and implications of both deferred and postponed retirement. Planning ahead, understanding the nuances of MRA, and evaluating personal health coverage needs are critical. For many, postponed retirement may offer a more beneficial path due to the preservation of health benefits and the potential for a higher annuity. However, each individual’s circumstances will dictate the most advantageous approach to take.

Reach Out to Us!

If you have additional federal benefit questions, contact our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciary (AIF). At PlanWell, we are federal employee financial advisors with a focus on retirement planning. Learn more about our process designed for the career fed.

Preparing for federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars through our webinar page. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out, and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting by contacting us.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.