Lifetime Income by Donating to Charity – Charitable Remainder Trust (CRT)

A Charitable Remainder Trust (CRT) is a little known secret that the wealthy have been using for years. The good news is you can use it as well.

A CRT allows you to:

- Receive a large tax deduction

- Eligible to roll tax deduction over 5 years

- Use the tax deduction to conduct a Roth conversion

- Create a lifetime income stream

- For 1 or 2 people

- Donate to charity

There are two main types of CRT’s:

- Charitable Remainder Annuity Trust (CRAT)

- Charitable Remainder Unitrust (CRUT).

We will be covering the CRUT. To maximize the CRUT, you will want to place a highly appreciated asset such as a stock or a highly depreciated asset such as a rental property into the trust.

Examples of highly appreciated assets would be stocks, private business interests, and private company stock. A highly depreciated asset is usually a rental property or commercial real estate. For stocks, you would avoid paying high taxes on the stock appreciation. For real estate, you would avoid paying taxes on the recaptured depreciation — learn more about capital gains tax on real estate.

One thing to note is that a CRUT is irrevocable, meaning you cannot unravel the trust or remove the assets once it has been established. You are permitted to change the charity through a trust amendment.

A CRUT will distribute a fixed percentage of the trust’s value. The trust is valued on January 1st of each year and the annual payment is paid quarterly. The payout rate must be at least 5% but no more than 50% of the assets in the trust.

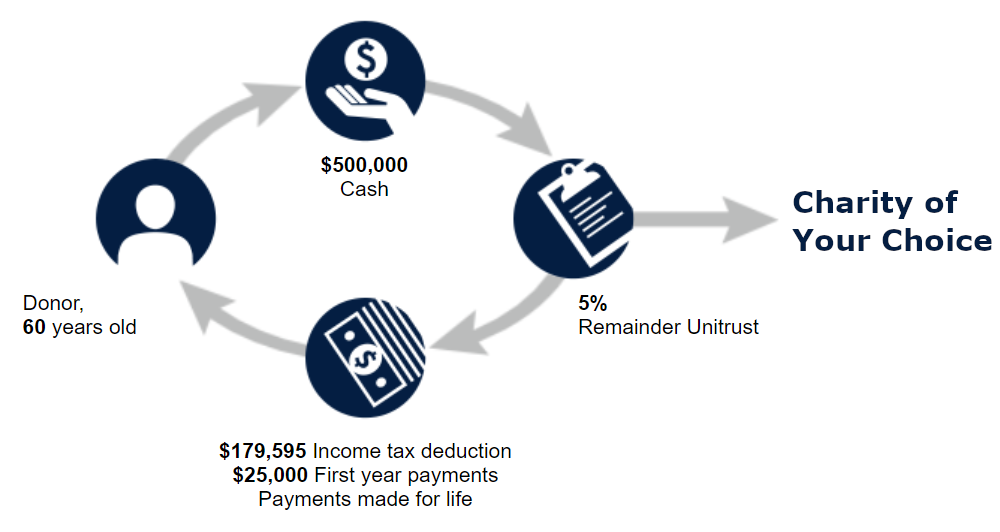

Depreciated Rental Example:

A donor age 60, is looking to exit their highly depreciated rental property.

- Rental Property Value = $500,000

- Cost-basis = $100,000

- Capital Gains = $400,000

- Federal = 25%

- State = 5%

- Capital Gains Tax = $120,000

Let’s say the donor chooses a lifetime payout rate of 5% on the life of one person. The donor would by-pass the $120,000 of taxes owed, receive a $179,595 tax deduction, and a lifetime income stream of $25,000/year that will vary on a year-by-year basis. The $25,000 income stream can increase or decrease depending on how the trust assets are invested. Ideally, you would see the trust value increase and thus the annual income paid would increase as well.

Massive Tax Deduction

So, what are you supposed to do with a tax deduction of $179,595 if you are unable to use the whole amount in year 1? You have two options: roll the tax deduction over 5 years or conduct a Roth conversion.

Tax Deduction Combined with a Roth Conversion

Conducting a Roth conversion will allow you to convert $179,595 of traditional retirement funds into a Roth IRA. This will allow your assets to grow tax-free without the burden of a required minimum distribution (RMD). If you’re looking for more ideas on reducing your tax burden, explore our Tax Strategy for Federal Employees.

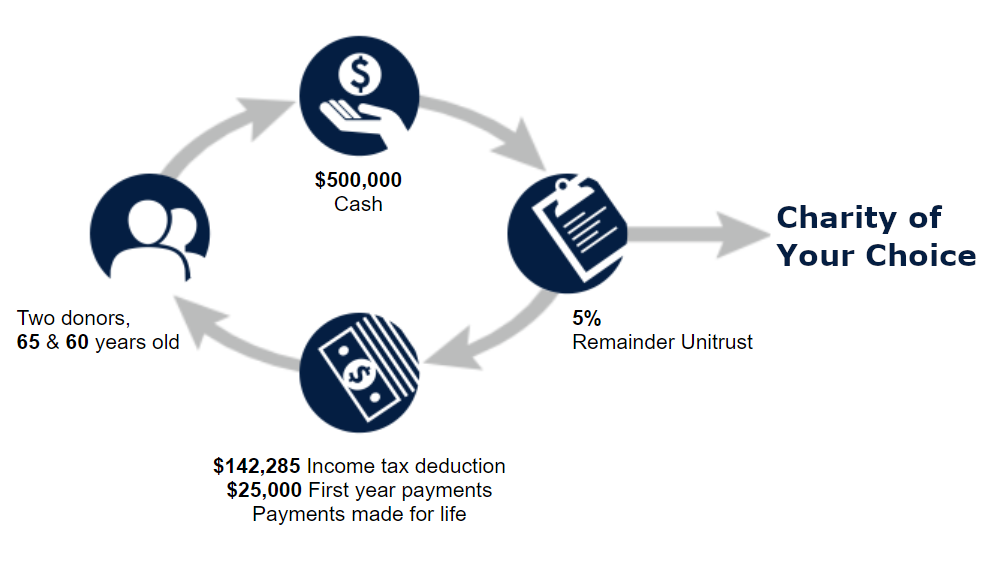

Highly Appreciated Stock:

A donor age 65 and 60, is looking to sell their highly appreciated stock.

- Stock Value = $500,000

- Cost-basis = $100,000

- Capital Gains = $400,000

- Federal = 20%

- State = 5%

- Capital Gains Tax = $100,000

- Annual Payment = 5% or $25,000 in Year 1

Let’s say the donor chooses a lifetime payout rate of 5% on the life of two persons. The donor would by-pass the $100,000 of taxes owed, receive a $142,285 tax deduction, and a lifetime income stream of $25,000/year that will vary on a year-by-year basis. Notice that the tax deduction is much smaller since the lifetime annual payments are for two people.

A Charitable Remainder Unitrust is an excellent planning strategy that not only allows you to save taxes while you’re alive, but also enjoy the fulfilling experience of giving to charity. If you have questions, please reach out to one of our Certified Financial Planners for a discovery meeting.

Reach Out to Us!

If you have additional federal benefit questions, contact our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciary (AIF®). At PlanWell, we focus on helping you navigate retirement as a federal employee financial advisor. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars through our webinar series. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out, and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting through our contact page.

Highly Appreciated Stock:

A donor age 65 and 60, is looking to sell their highly appreciated stock.

- Stock Value = $500,000

- Cost-basis = $100,000

- Capital Gains = $400,000

- Federal = 20%

- State = 5%

- Capital Gains Tax = $100,000

- Annual Payment = 5% or $25,000 in Year 1

Let’s say the donor chooses a lifetime payout rate of 5% on the life of two persons. The donor would by-pass the $100,000 of taxes owed, receive a $142,285 tax deduction, and a lifetime income stream of $25,000/year that will vary on a year-by-year basis. Notice that the tax deduction is much smaller since the lifetime annual payments are for two people.

A Charitable Remainder Unitrust is an excellent planning strategy that not only allows you to save taxes while you’re alive, but also enjoy the fulfilling experience of giving to charity. If you have questions, please reach out to one of our Certified Financial Planners for a discovery meeting.

Reach Out to Us!

If you have additional federal benefit questions, contact our team of CERTIFIED FINANCIAL PLANNER™ (CFP®) and Chartered Federal Employee Benefits Consultants (ChFEBC℠). At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars here! Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out, and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting here.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.